Screening: Brazilian consumer discretionary

Recently, I have found many companies in Brazil that seem to have attractive valuations. My latest articles all address that topic, and I continue to screen and review companies in the country.

This time, I carried out a screen of the consumer discretionary sector. It is not a deep dive on each of the companies, not even a shallow dive. Just looking at each pond from the shore, to notice the shine of a golden pebble or the rotting smell of poisonous algae. I think I have seen some shining pebbles under some of the ponds.

Because they are particularly exposed to the consumer and economic cycle, discretionary names can get quite cheap and quite expensive with the same ease. In the current context, where there is a lot of uncertainty around the global and Brazilian economies, I hope to find some babies thrown out with the bathwater: durable brands and business models that are discounted even assuming the economy worsens.

This is what I found:

Potentially undevalued (3 names)

Potential deep value (2 names)

Fair with quality (1 name)

Fair, regular business (8 names)

Pricey, regular business (4 names)

Too levered (6 names)

Vamos la!

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. I may own or later purchase some of the stocks mentioned in this article.

The opportunity set

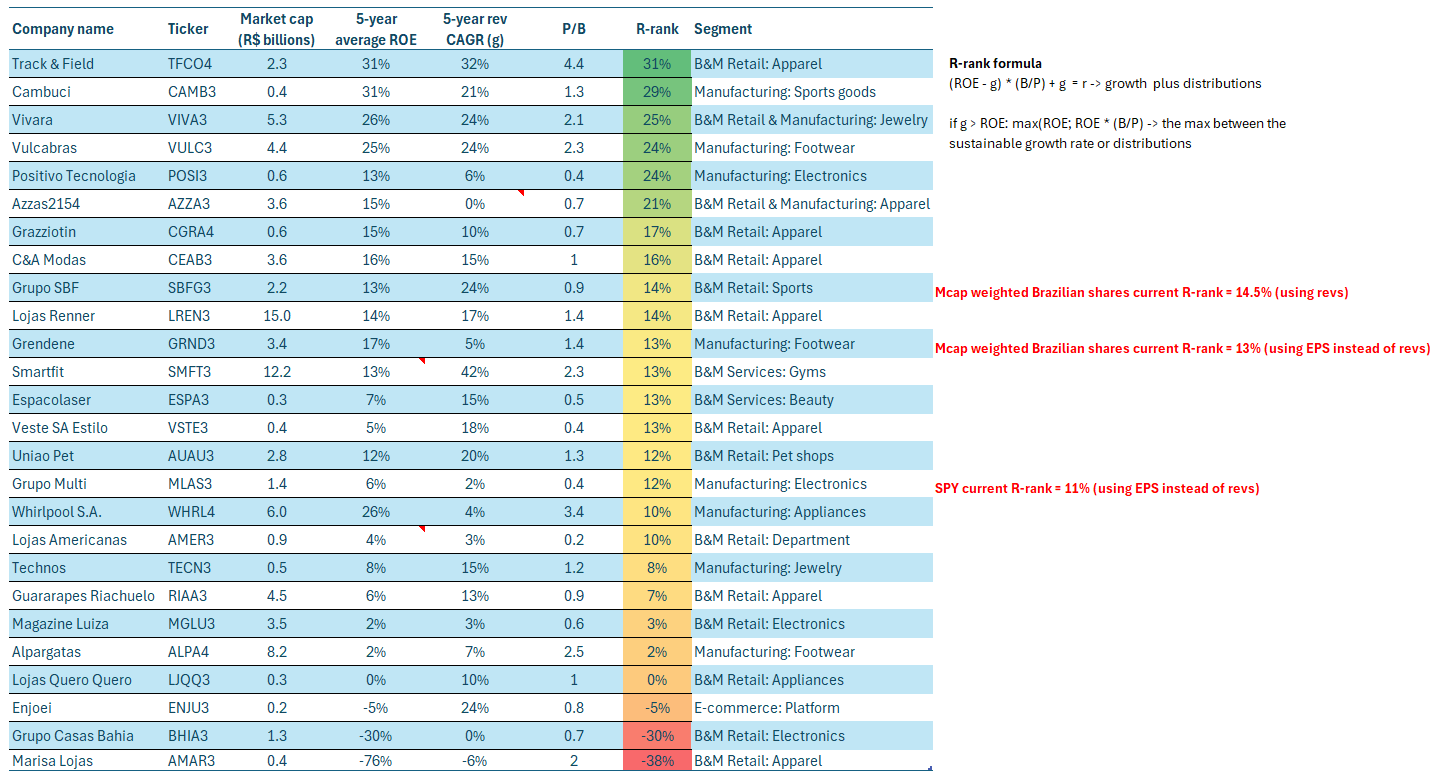

Following the structure I recently explored on an article on screening, a lot of companies in consumer discretionary in Brazil seem quite interesting, both compared to the SPY and to all Brazilian companies in general.

There have been plenty of fast growers (SMFT3, TFCO4, VULC3, VIVA3, SBFG3, VIVA3, CAMB3, AUAU3, VSTE3, LREN3, CEAB3, all above 15% CAGR), considering that Brazilian inflation has been around 4% per year since 2021.

Also a few companies with impressive ROE averages (TFCO4, CAMB3, VIVA3, VULC3 all above 20%).

When the growth rate is larger than the ROE (you could not finance that level of growth with equity alone), I select the smaller between ROE (the sustainable growth rate) and the potential distributions to equity (ROE divided by P/B).

Of course, the formula by itself does not say much beyond ‘there might be something here’. The r-rank by itself is nothing but an early indication of potential. The next step is to actually look at the names with a more discerning eye, which is the purpose of this article. As an example, my recently covered Alpargatas, arguably one of the strongest companies in the list above, ranks almost at the bottom of the table because it presented large write-off losses between 2022 and 2024.

When looking at the names more closely, but still within a screen-level review, I focused on these qualitative and quantitative aspects:

Adjust earnings to represent operating factors and not others, like one-time gains, mergers, etc

Based on these, re-estimate equity returns today

Calculate capital returns on net tangible assets today to compare with equity.

Compare growth in revenues with growth in assets and in operations (number of stores, etc.) to separate capital-accretive growth

Speculate on a forward-looking sustainable growth rate

Estimate exposure to the consumer discretionary cycle

Estimate operating leverage

Account for financial leverage

Re-estimate the distribution yields and sustainable growth rate

Re-rank opportunities

Below, you can find my company classification by opportunity bucket (or lack thereof), plus the full spreadsheet.

Potentially undervalued (3 names)

Potential deep value (2 names)

Fair with quality (1 name)

Fair, regular business (8 names)

Pricey, regular business (4 names)

Too levered (6 names)