[free] My current screening setup

- Opticorvm libri sex, 1613.jpg")

Over the past few months, I have been making my idea-generation process more systematic.

Historically, many Quipus articles started from curiosity, reader suggestions, or serendipity. This has served me well, but it can be improved. Attention is not only all we need, it is all we have, and it should be put to the best possible use.

That’s why, in this piece, I wanted to briefly discuss how I screen. The goal is to share my method and get some new ideas.

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product.

Attention, speed, sensitivity, specificity

The goal of screening is to tell us where to concentrate our attention, instead of focusing blindly on whatever name comes our way. It’s a way of estimating which haystacks have more needles, or which ponds have more fish.

Attention and focus are very related to time and speed. A faster screen leaves more time for researching the valuable names. However, the screen also has to be complex enough so as to be effective, catching the opportunities.

Some scientific test terminology comes in handy with this. A test is sensitive if it catches most positives. A test is specific if it correctly discards most negatives.

Specificity and sensitivity are usually in a trade-off. Make the test too stringent, and you only get 5 out of the 10 opportunities within 100 names. Make it too lenient, and you get the 10 opportunities, but also 10 that look like so but are not.

I personally prefer to sacrifice specificity for sensitivity; that is, I want to catch all potential opportunities, even if that also means catching some that look like opportunities but aren’t. The reason is simply that I can be more stringent later in the research.

What I look for: fundamental sources of return

The screen should be tailored for stocks matching a particular style or strategy. The key question is what kind of companies the screen should surface, and more importantly, which characteristics distinguish those companies.

In my case, as a fundamental value investor, I look for durable streams of earnings that can be distributed to me or invested at high returns in the business.

In an article from last year, I explained why this is so in more detail. I have opened it for one week so that you can read it for free.

Very succinctly, though, a stock only has three sources of returns:

Dividends paid from earnings or from retained capital.

Growth in earnings, which may come from revenues, margin expansion, deleverage, buybacks, or other form of investment (CAPEX, M&A).

Growth usually requires capital/investment, meaning it is a trade-off with dividends.

Multiple expansion, representing the market’s improving outlook for future earnings.

First pass: one metric to rule them all

With this in mind, my ideal stock has two characteristics:

Stable earnings at a low multiple.

The ability to grow without much capital (high incremental capital returns).

If this had to be summarized in three fundamental metrics, they would be P/B, past revenue growth, and ROE.

These can be combined into a single fundamental return score:

(ROE - g) x (B/P) + g = r

where g = 5-year revenue CAGR; ROE = 5-year average return on equity; B/P = inverted price/book multiple

The larger the r (expected return), the more promising the name

The equation if read out low:

ROE - g is the return from equity after paying for growth (in % terms). This assumes that growth does not affect margins, and that ROE is constant. These are strong assumptions which we can review in the second pass and in later research.

(ROE - g) * B is the actual distributable earnings figure, in dollars. That is, how much money we have after paying for growth. When we divide by P, we get a distributable yield. This assumes either the yield is distributed (dividends) or that the P/B multiple stays constant.

g (as a %) becomes a yield or return if we again assume that margins are stable and that the multiple is stable. If the company earns 5% more and the P/E stays constant, then the stock price goes up by 5%.

If I had to screen based on one thing only, it would be the above. This is also a great place to start looking for sectors/countries.

Of course, the formula is not a valuation model and is laden with assumptions (which I question in the second and third passes). It is simply a screening ranking score, nothing less, nothing more.

Second pass: additional metrics and qualitative factors

However, this is too simplistic and therefore does not work as a good test. It may be a good ranking system, or a first sieve mechanism, but it is not enough. Just by adding a little nuance, I can get a lot more. The key aspect here is to transform a backward-looking view into a forward-looking intuition:

Idiosyncratic factors: A five-minute read business introduction from ChatGPT or Claude can go a long way in describing the business and the industry. From this, one can get a qualitative handicap on earnings durability and potential growth.

Key factors include:Operating leverage: above, we assumed that margins are flat with revenue growth, but this is usually not the case in the short to mid-term.

More generally, if margin volatility is high, we would want to know why and adjust accordingly.Industry and country cycle: a company that grew a lot in the past 3 years but is very exposed to consumer discretionary may also shrink during the next crisis.

Business quality: does this seem like a company with a moat and some barriers to competition or that does business better than competitors? The most indicative factors are high (and/or growing) returns on capital and high margins.

Earnings and ROE sanity check: Armed with the above idiosyncrasies, review a long-term earnings table to check whether current earnings metrics make sense or are affected by one-time factors. Try to discriminate for cycles and add a fudge factor. Another option is to use averages.

Normalize growth: Same idea, if the business has been growing at 20% CAGR for 5 years, is that durable? Worse, is that mean-reverting? Is that potentially affected by an industry or country-level cycle?

Capital structure (ROIC, leverage): What is the return the company earns on all of its capital, and how does it compare to ROE? Some companies can improve their ROE by adjusting their capital structure.

Past capital allocation: Have managers/directors actually distributed dividends? Have returns on capital increased over time? What does it tell about the previous expectations?

Once this round is done, I have a much more nuanced view of the selected companies. The ranking has changed, and is no longer only quantitative, because factors like operating leverage or business quality cannot be captured in a score. Most important for the next stage, for each company I have a set of key questions/drivers.

Third pass: Research key factors to kill ideas

The next stage is to incrementally ask key questions that would make me kill this idea. Conversely, the longer the idea survives, the stronger my confidence in it.

Originally, the key questions come from the screening above. For example, explain what happened during margin volatility periods. Paint a better picture of the components of earnings and their durability. Check that the leverage and margin figures are not contaminated by non-recurring factors. Check comments on capital allocation policies in the future, etc.

As I review the materials, more questions arise, and the process can technically go on to indiscriminate depths. This is technically not part of screening anymore, but it is still informed by screening.

A recent example

A few weeks ago I wrote about Brazilian residential real estate developers.

_-_Opticorvm_libri_sex,_1613.jpg){kind=link}

The screen looked really nice, as seen in the table below. Using the median figures for the sector, we get:

(ROE - g) x (B/P) + g = r

(41% - 27%) x (0.3) + 27% = 4% + 27% = 31%

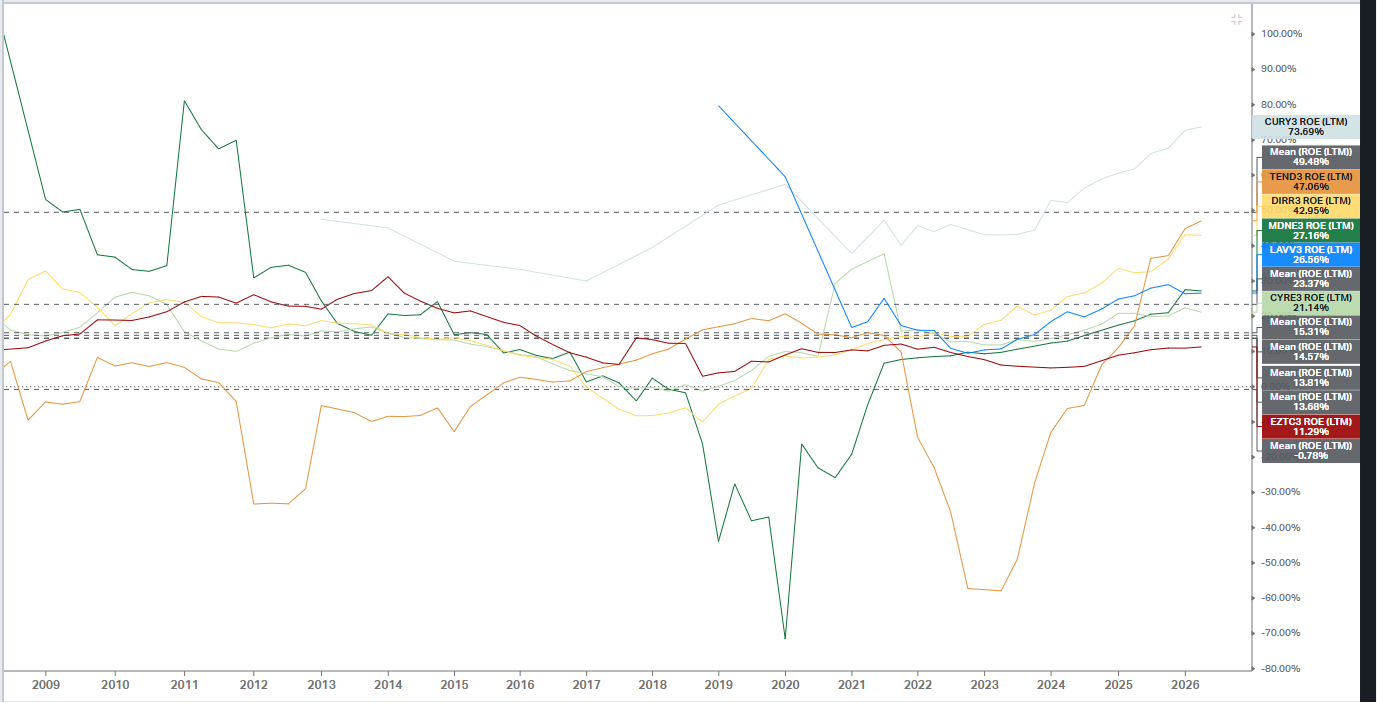

Of course, that is only the first signal, not a confirmation of anything. The next step is to do a sanity check. One very basic check is that real estate is cyclical, meaning you can get very differing growth and return on equity at different times. Indeed, that was evident from a simple review of ROE over time and stock prices (with some names getting too close to 80% negative ROE, meaning almost wiping out the equity during bad years).

But overall, the question remained valid: returns on equity were really high in some cases even on a very long-term average basis, and so was growth, so some research could present an opportunity, which ended up becoming the article.

This case is a good example because the screen only surfaced a salient market situation (something scoring a 30% return expectation), which ended up spurring a much more detailed research project.

What do you think?

As I said, I’m new to screening, and my method might have a lot to improve.

Do you screen at all? If not, how do you come up with new ideas?

How do you screen?

Do you see any obvious problems with this method?

New to Quipus?

Go to the About Page to find several additional free articles.

For the full view, 50+ articles covering dozens of industries and companies from emerging markets in depth can be found in the Index