2Q26 Portfolio Review

After every quarter, I provide a review of the performance and positions of my two personal accounts (IBKR and Argentina). I think this provides readers with more context and transparency about the way I think and act as an investor myself. Most of the names for which I have positions have been covered in the blog. This article reviews 2Q26.

You can visit previous reviews in the Index

The article is organized by account, posting the historical returns, 2Q26 returns, sources of the quarterly returns, the changes in positions during the quarter, and finally, the ending positioning.

Before beginning, I wanted to thank all of Quipus Capital’s readers for your support, especially those who have upgraded monthly or yearly. The blog has more than 2,000 readers. Writing and researching for Quipus is a great pleasure.

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product.

Aggregate comment

The quarter was simply terrible for me. Not only did I lose most of what I had gained earlier in the year, but I did so while (and partly because) the market was roaring through a raging bull. What’s worse, a large part of this underperformance cannot be shrugged as temporary market vagaries, because a large percentage of the loss happened in options.

Lesson learned: being stubborn doesn’t go well with short-dated options. Either not use them, or be able to change your mind quickly.

Other sources of loss for the quarter included themes on which I am more confident, and that above all, are at least potentially recoverable: Brazil gave up a part of its gains earlier in the year, and so did oil and other materials. Almost no stocks I own had positive returns for the quarter.

In terms of focus, I am definitely shifting to value at its own catalyst, screening more from cheapness than from a structural thesis on the sector.

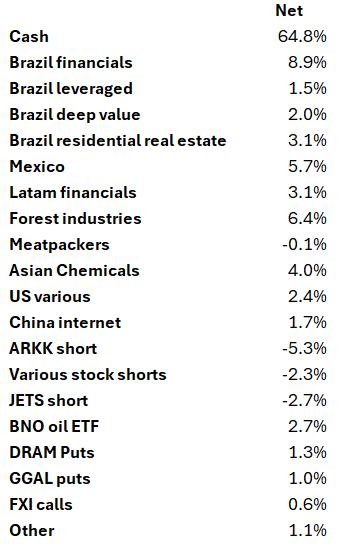

I remain happily uninvested though (cash 56% average weight on IBKR, 50%+ weight in Arg), given my relatively bearish views.

IBKR account 2Q26

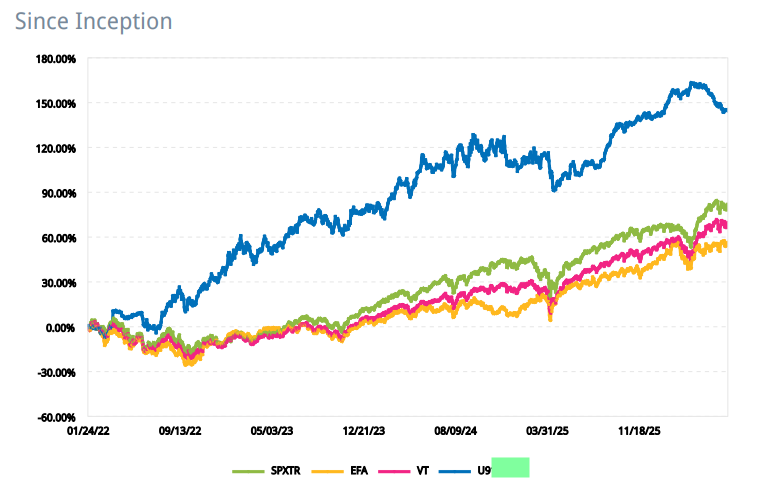

Q2: -7.1%%; YTD: 1.4%; 1 Year: 18.6%; Since inception (Jan22): 144.6% (CAGR 22%)

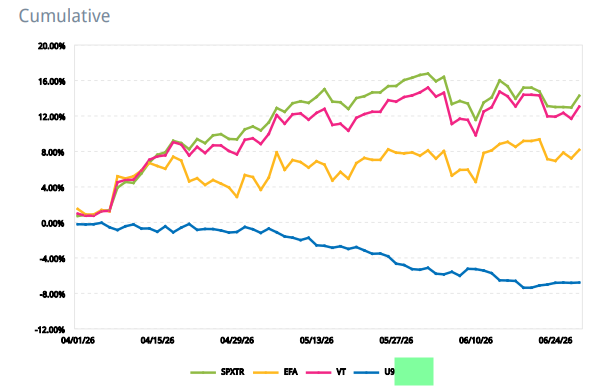

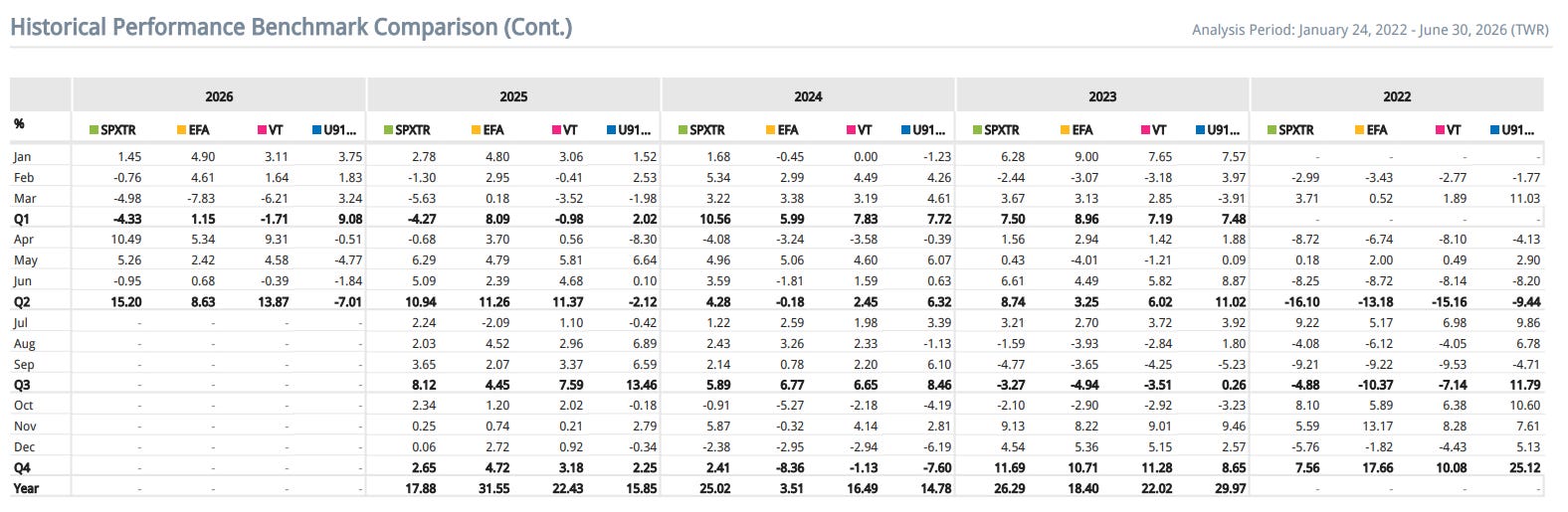

Historical returns

The first image below shows the performance of the account by month and quarter (“U91..” column) compared to three benchmarks (SPXTR, EFA, and VT). The second image shows the same comparison in chart form, ending in 2Q26.

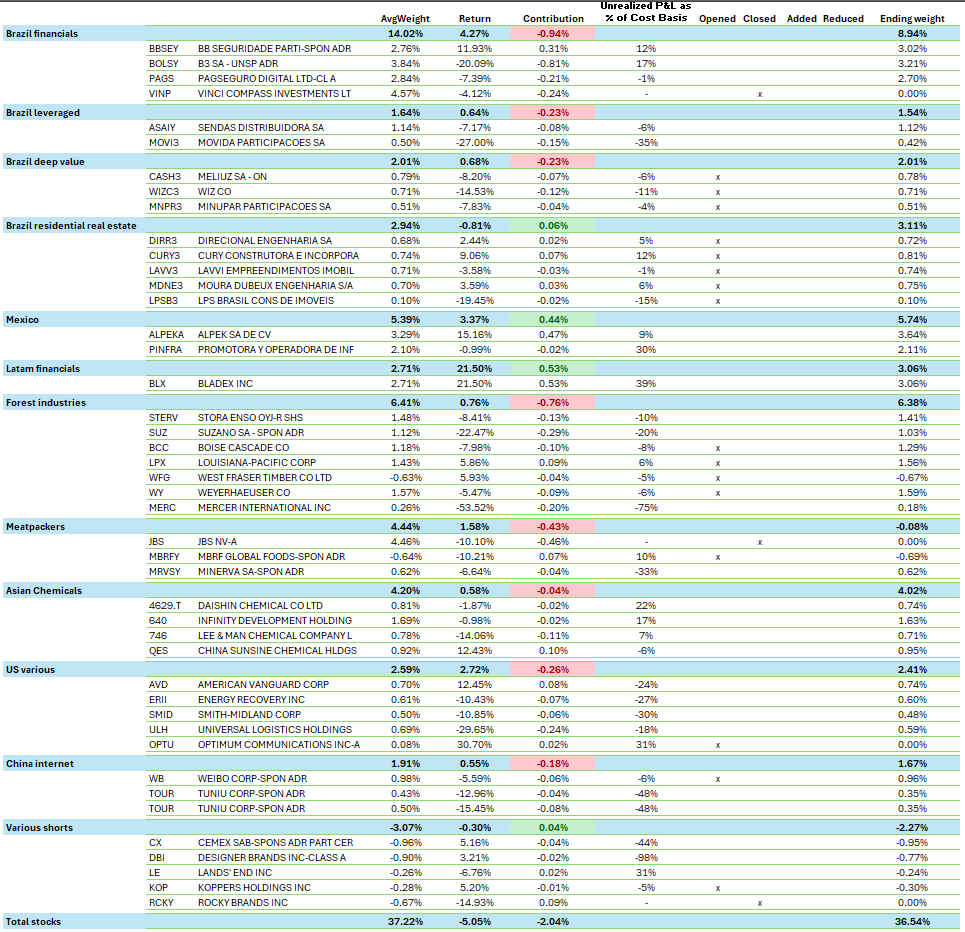

Return sources for the quarter and changes in positions

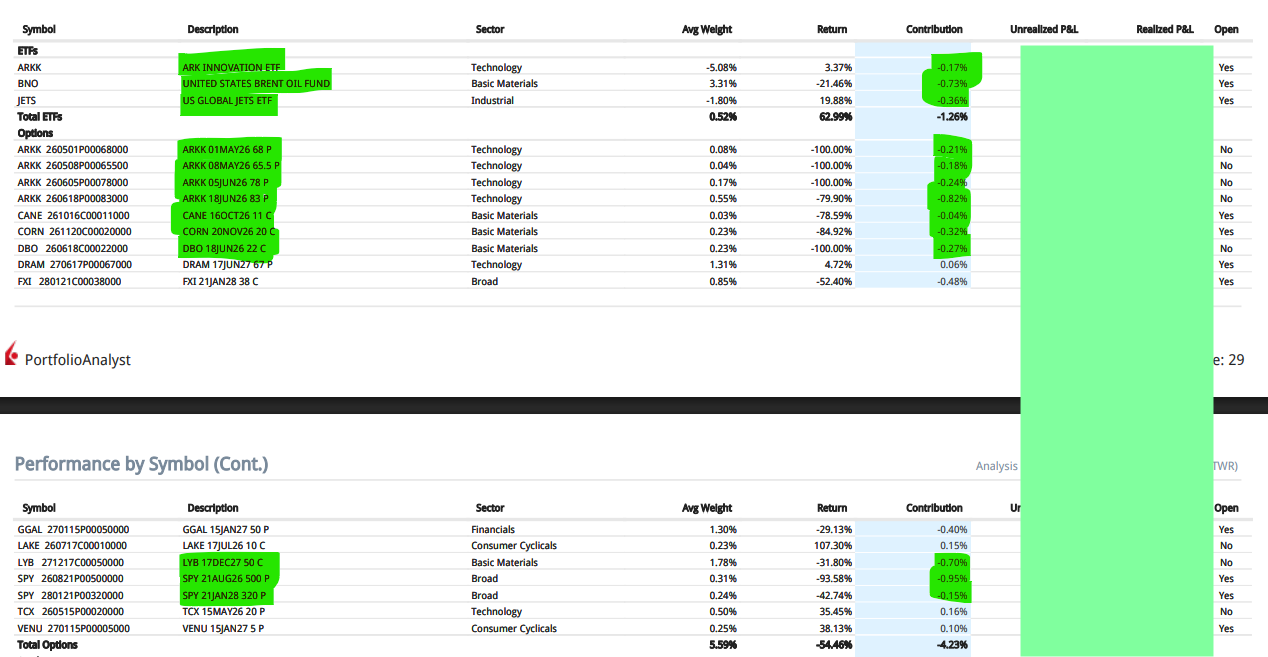

I am a Hormuztard

The most important way in which I lost money this quarter was by remaining bearish on the market and bullish on oil. To make things worse, I expressed these views excessively via short-dated options that got whacked when the market exploded to the upside and oil to the downside.

As seen in the table above, I lost 5.14% in the positions marked in green. They are short the market (ARKK and SPY puts, ARKK ETF short), short JETS (airline ETF), long oil (BNO ETF, DBO calls), or long oil-related (LYB calls, CANE and CORN calls).

I don’t think my general idea was a mistake, and it would have been really hard to predict both a collapse of oil and a raging bull market (SPY up almost 20% in the quarter) as global inventories of fuels continued to collapse, the Strait remained only 30% operational after 4 months of conflict, and the US arguably lost the War.

However, where I see a huge mistake is in taking large positions in short-dated puts, such as almost 1% of the account in an SPY 500 put with expiry in August 2026, or a total of almost 1.5% of the account in several ARKK puts with expiries in May and June.

I remain convinced that, now even more than before, being long oil is an opportunity, so I keep both the ARKK and JETS shorts, and the BNO long, but I’m not adding to puts, especially short-dated.

Other options

I also got whacked in GGAL (largest Argentinian banks) put options (expiry January 2027) as the Argentinian stock market rallied with the rest of the market. I remain bearish on the country and its market, so I have not sold the options, but will probably not add.

Another terrible point was FXI (China ETF) calls (expiry January 2028). It seems that almost everything China-related has been disastrous this year. I don’t have a super strong China view, simply that it seems odd that the country running trade surpluses and leaping in technology is the one being left for dead. This is a long-dated option, so I can wait.

I opened a DRAM (memory stocks ETF) put (expiry June 2027), for the same reason that I had bought long-dated puts in EWY (Korea ETF) and SLV (silver ETF) earlier in the year: a chart that goes up vertically will also probably go down vertically. I know nothing about memory producers, except that it is a cyclical industry and that everyone and their mothers talk about the bottlenecks.

Stocks and themes

In aggregate, the stocks added a loss (around -2% contribution), and they obviously underperformed the markets meaningfully (aggregate return of -5% versus the markets up 10%/20% depending on the index).

Brazilian financials

BOLSY had a rough quarter, in line with a falling Brazilian stock market. Being an exchange, it is leveraged to those movements.

I closed my VINP position because the company’s balance sheet position has deteriorated, I don’t agree with recent capital allocation decisions, and the window for PE to have a revival in Brazil is lengthening. I explained more in this X post.

Brazilian leverage

The Brazilian levered names did not perform this quarter, potentially because Brazilian sovereign debt markets cratered (higher rates) because of political risks. Despite this, the SELIC and interbank rates are still expected to fall.

Brazilian deep value

New varied category, initiated this quarter.

Brazilian residential real estate

Another recent category.

Forest industries

Added some positions from wood products in NA. Suzano has been hit by higher costs (fuel), a more expensive BRL (lower revenues per ton exported), and falling prices in China.

Meatpackers

Sold my JBS position after the review of the sector, and added a short on MBRF

Ending positions

Argentina account

Q2: -1.96%; Since inception (Oct20): 261% (CAGR 25%)

As always, I must warn that the returns on my Argentinian account are harder to calculate. My broker in Argentina provides only terrible and broken Excel reports in Argentinian pesos, requiring a lot of cleaning and conversions to USD. Further, the investable universe is much smaller (only Argentinian stocks and a few hundred depositary shares from abroad), and I have an incentive to remain fully invested because of inflation or the risk of holding USD cash in a non-US jurisdiction.

To put an example of the unreliability of the figures, the return for the quarter was negative, and yet the aggregate return increased (in 1Q26 I had reported 255% since inception). This probably has to do with the fact that the calculation is money-weighted.

Finally, the Argentinian account is now about 20% of the IBKR account, as I don’t add to it, but rather take from it to pay for expenses.

During the quarter, the three Brazilian stocks I own in the account- LREN, XP, and PAGS- went down. I simply sold XP, PAGS, and LREN to pay for expenses, and bought some Weibo to use part of the cash I had.

Given the size of the account (now less than 20% of the IBKR account), the smaller universe, and the difficulty of calculating returns, I will no longer report these results.