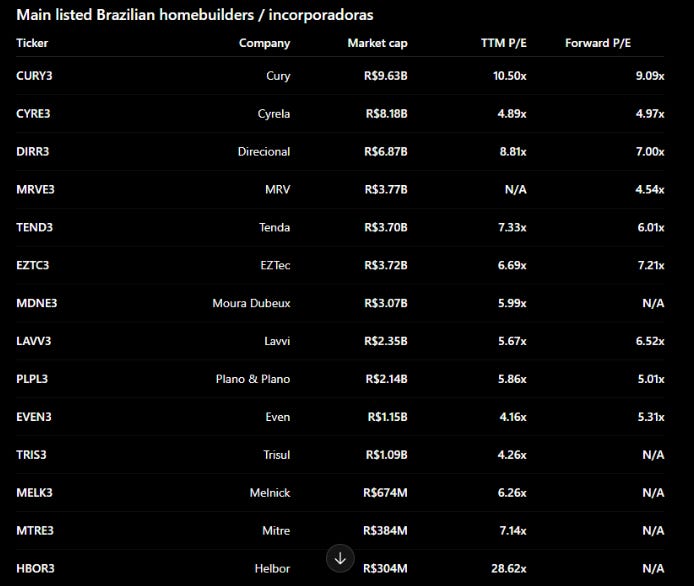

Brazilian real estate developers: MSD multiples

$CURY3, $CYRE3, $DIRR3, $TEND3, $EZTC3, $MRVE3, $MDNE3, $LAVV3, $PLPL3

Screening for cheap multiples, I ran into the Brazilian real estate developers (called incorporadoras in the country). They definitely screen at very low multiples, even for forward estimates.

But being a cyclical guy, I was not going to be convinced by a low multiple alone, let alone in the mother of all cyclical industries, real estate.

Indeed, the stocks look quite cyclical, and they seem to be falling from a recent peak. It is therefore very reasonable for them to look cheap on a look-back earnings multiple basis, but still get sold off. This looked just like another cyclical top.

However, some other things caught my attention:

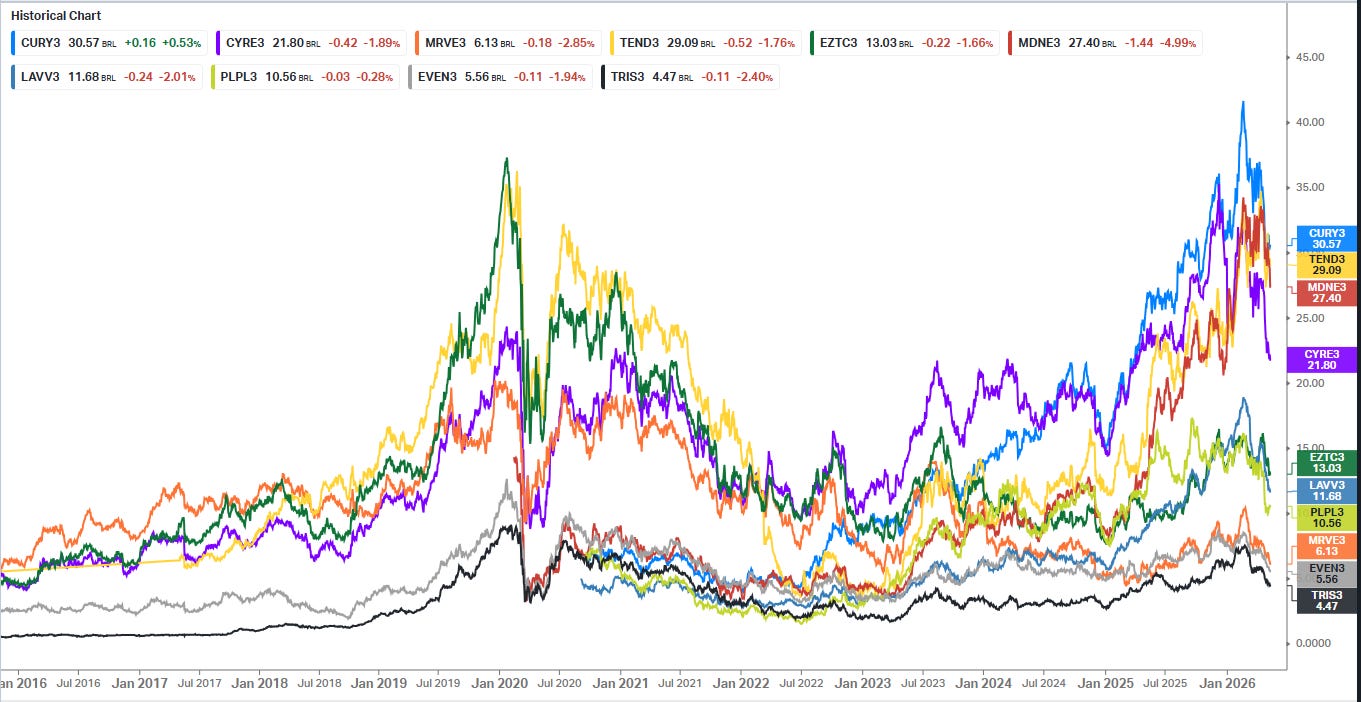

The Brazilian real estate developers have performed very well between 2022 and 2025. This seems contrary to intuition, given that rates have been up in Brazil. High rates are usually poison for real estate developers.

Similarly, the stocks of the developers are down even though, so far into late 2025, early 2026, the consensus was for lower rates in Brazil.

When we divide sector stock prices (as represented below by the $IMOB.SA index, which also includes real estate ownership) by the USDBRL exchange rate, the sector is at a recent peak but remains far from previous peaks in Brazilian real estate.

Armed with that curiosity, I analyzed the sector, and this is the resulting article.

It analyzes the drivers of the cycle, which is obviously very affected by hard-to-predict macro factors like credit and employment, by providing the granularity needed to create scenarios that are not as simple as economy good, economy bad.

Of course, I cannot know what will happen with the economy, but luckily, I don’t really need to. The article compares the companies’ market cap today (or at some point in the future if revisiting) with estimates of fair value based on operations under different scenarios, including an analysis of financial stress (key for developers) and operating leverage at different construction levels. We can use those estimates and commentary for each company specifically to speculate on what the market is pricing and whether we agree with those views.

Hope you like it!

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. At the time of publication, I do not own, but may later purchase, securities mentioned in this article.

Index

The drivers of the real estate cycle

Funding and programs: MCMV, FGTS, SBPE, livre

Employment and cyclicality ahead

Valuation models

Key warnings on construction accounting

Operational KPIs of the builder

Financing stress: acid test model

NAV model

Scenario profitability model

General conclusions

Company notes and commentary

$CURY3, $CYRE3, $DIRR3, $TEND3, $EZTC3, $MRVE3, $MDNE3, $LAVV3, $PLPL3

The spreadsheet for the models and the data collected can be found in the Annex to this article.

Drivers of the BR residential real estate cycle

Credit availability is the main driver of the residential market.

Housing credit is heavily regulated under several programs, each with different funding sources.

How these funding sources behave end up regulating the residential cycle more than general financing conditions (like SELIC).

50%+ of the market is driven by the MCMV program, which obtains funds from a workers’ severance fund (FGTS). This type of credit is therefore driven above all by the aggregate employment level and worker salaries.

Another 40% of the market is driven by the SFH program, which derives funds from poupança deposits. Because of poupança’s rate mechanism, SFH credit is inversely correlated to SELIC (contracts when SELIC goes up).

A small by growing share of the market is fairly unregulated (credito livre). It gets funding mostly from mortgage securitized vehicles called CRI. Availability depends on general credit apettite more directly.

Like in almost any other real estate market, credit availability plays the key cycle-regulating role in the Brazilian residential market. When credit is abundant, there’s ample demand, and when it is not abundant, demand dries up.

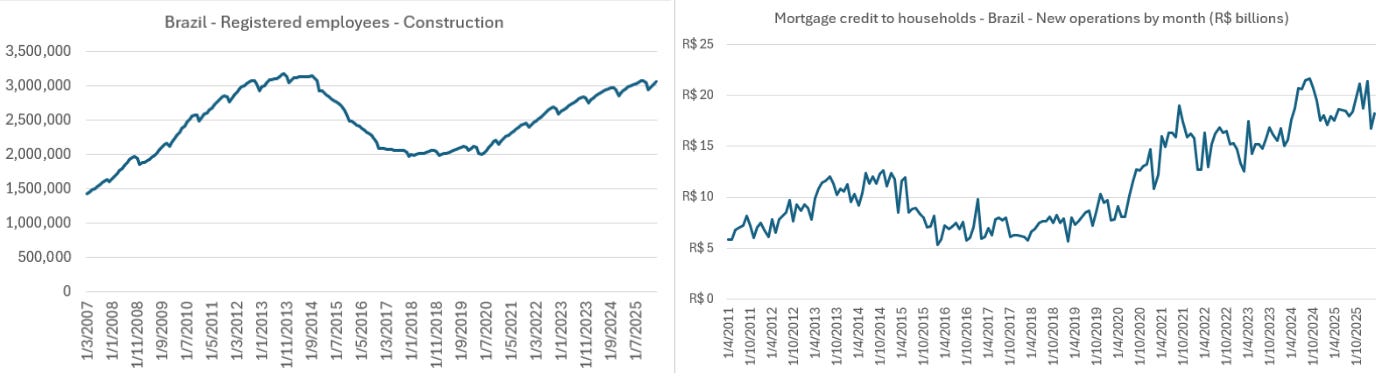

The relationship seems pretty evident in the charts below, which compare construction employment (left-hand) with monthly mortgage credit creation (right-hand). (Note: R$1 in 2014 is about ~R$2 in 2026 due to inflation and depreciation, and therefore the two peaks of the right-hand chart are of similar inflation-adjusted value).

However, the credit market for real estate in Brazil are not tightly coupled to general financing conditions, like the reference rate SELIC, or bank lending apettite.

Rather, housing credit availability and costs move according to different government programs and home-ownership financing frameworks. These financing frameworks determine specific funding sources, where the funds should be allocated, and at what cost.

To understand the cycle we need to analyze each of these funding sources and lending programs.

Funding and programs: MCMV, FGTS, SBPE, livre

Man, once you start to analyze a regulated sector in Brazil, you get a salad of acronyms! However, fear not, it is simpler than it seems.

If we were to mix it with another cultural snippet, maybe from the Chinese love for short phrases, we could call the Brazilian residential real estate system the ‘Three sources and three programs” (三源三项).

Three sources of funds determine where the money comes from to finance the real estate credit (FGTS, SBPE, livre), and three programs determine the conditions under which credit is provided (MCMV, SFH, SFI).

Three sources

FGTS (Fundo de Garantia do Tempo de Serviço)

The FGTS is the fund that guarantees and manages the severance savings of all registered workers in Brazil. Employers pay 8% of the salary of the worker, per month, to the FGTS. When the employee is fired without just cause, for example, because the business doesn’t need the worker anymore, the FGTS pays him the severance. The worker can also get his funds if/when he retires.

The funds of the FGTS are primarily invested in real estate credit, primarily through the MCMV program. The FGTS does not retain the credit risk, which is transferred to the Caixa Econômica Federal, a state bank and the leading mortgage lender in the country (60/70% share). That is, the FGTS lends to Caixa, so that Caixa can lend to MCMV borrowers.

Because FGTS is funded from workers’ paychecks, it connects the employment market with the residential housing market. In this sense, it is incredibly procyclical: When the economy is expanding, unemployment falls, and worker salaries improve, leading to the FGTS receiving more funds, and therefore lending more to the residential market. However, when the economy shrinks and the number of workers falls, the FGTS will naturally shrink, its liquidity needs will increase, and it will therefore reduce the availability of credit, leading to a credit crunch, which worsens the economic slump.

The recent employment and salary expansion explains a large part of the boom in residential real estate of the last 3 years.

An additional challenge that the Brazilian regulators will eventually need to solve is what to do with the FGTS when the number of retiring workers is higher than the number of incoming workers.

SBPE (Sistema Brasileiro de Poupança e Empréstimo)

The SBPE system obtains its funds from a specific bank investment product called caderneta de poupança (savings book, let’s call it), aka poupança. Banks are mandated to dedicate 65% of their poupança deposits to real estate credit at mandated rates (credito direcionado).

Most modern savings products in Brazil today are tied to the CDI (the interbank rate), which is highly sensitive to the SELIC (the Central Bank reference rate).

The poupança rate follows a different scheme, which is more countercyclical and “stable”. When SELIC is above 8.5% a year, it pays less than SELIC, and when it is below 8.5%, it pays above. In addition, poupança is exempt from income taxes.

The effect is that poupança deposits expand when SELIC rates are low but contract or wane when rates are high, because people make more money on interbank-tied products.

Whereas FGTS is employment-cyclical, SBPE is rates-cyclical. In some sense, SBPE and FGTS tend to complement each other, because SBPE (poupanca) will increase with low rates, which are expected during a high-unemployment period, and will decrease during a high-rates/high-employment period, when FGTS takes the lead.

We can see this dynamic during 2020/21 when unemployment was high, and rates were low, and therefore SBPE grew (people migrated to poupança), whereas as employment and rates increased, FGTS came to the lead and SBPE shrank. Of course, a high-rate, high-unemployment period is the double-whammy of the system.

Finally, the SBPE system has recently come under reform. From 2027 onwards, the investment mandates will change. Banks will be required to have real estate credit products for 100% of their poupança deposits, but can then apply the poupança funds to whatever lending they desire. The difference in the system is a) increasing the share of poupança that goes to real estate credit; and b) separating the real estate product from the bank that generates poupança deposits.

Livre

Livre refers to any other source of funds that is not mandated to be invested in a specific real estate application.

Banks can lend to mortgage borrowers using any funds they desire, into any program/credit vehicle they desire, but of course, then the cost of credit will probably be the market cost.

The main vehicle for livre real estate credit is securitized mortgage instruments called CRI (Certificado de Recebíveis Imobiliários). CRI somewhat match the maturity structure of mortgages, and are exempt from income taxes on the interest for individuals.

Today, livre is a rather marginal portion of the residential credit market, but it is possible that it will replace part of the SBPE system as the reforms are implemented post-2027.

Three programs

The three programs or regulatory frameworks under which people can borrow to buy a house in Brazil are basically divided according to income class and property value, going from MCMV (low to middle class), SFH (middle to upper middle), and SFI (others).

MCMV (Minha Casa, Minha Vida)

MCMV is a subsidized-rate and sometimes subsidized-principal program geared towards low and middle-income families. It has existed since 2009, with a short name change (Casa Verde e Amarela) during the Bolsonaro administration. As explained above, it is mainly funded by the FGTS and managed by the Caixa Federal.

Rates can be very attractive, at 4% in the lowest range and 10% at the highest. It is divided into four segments (Faixas 1 to 4) based on the family's gross monthly income (going from as low as R$2,500 or ~$500 to R$13,000 or ~$2,500) and the price of the property (~$40/50,000 to ~$125,000). Depending on the faixa, the subsidies to rate and principal increase (lower income, higher subsidy). Given that the average salary in Brazil is R$3,700/month, MCMV covers most of the Brazilian population.

MCMV is also highly attractive for developers because the Caixa will “partner” with the developer (credito associativo) and provide funds during construction. This is obviously very helpful for developer cash-flows, which otherwise need to finance the construction themselves with equity or debt.

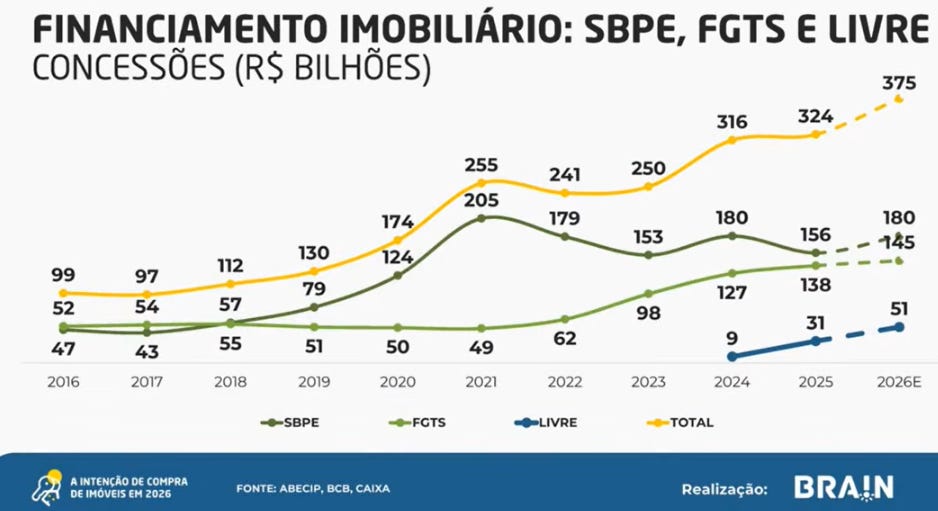

Given the context of a decrease in SBPE (see below), the expansion of the FGTS, and the facilities for developers and borrowers, it is unsurprising that MCMV represents the totality of the residential real estate construction segment growth between 2022 and 2025. Because of its connection with FGTS, MCMV is pro-cyclical with employment.

SFH (Sistema Financeiro da Habitação)

The SFH system is the next tier of directed credit. It can finance units up to R$2.5 million, or ~$500 thousand, which is a lot in Brazil: a middle-class, or padrão media apartment in São Paulo, can cost R$700 thousand.

The funds come primarily from the SBPE (i.e. poupança) system.

The rates are not subsidized, but capped at 12%, which is why banks need to use the poupança funds to finance this type of credit, which, under current market conditions, would otherwise have negative margins.

Of course, the average SFH loan is probably not close to R$2.5 million but rather to the MCMV ceiling of R$600/800 thousand. This segment of the population has been somewhat excluded from the attractive credit conditions of MCMV.

SFI (Sistema de Financiamento Imobiliário)

The SFI is the equivalent of the livre funding source on the lending side.

Not only can banks lend to other types of projects that are not residential, but they can also charge whatever rate they desire. As mentioned under livre, most of the financing comes from CRI instruments.

Cyclicality ahead

Because FGTS/MCMV depends on employment and unemployment is at record lows, it is unlikely to expand as it did in 2022/25. It can either expand more moderately based on salary growth and formalization, or contract because of higher unemployment That is a neutral to negative outlook.

SBPE/SFH and Livre/SFI depend more directly from credit conditions, of which employment is only a factor. The best scenario is lower rates that are not caused by a recession. Still, in a higher-unemployment, lower-rates scenario, this type of credit (and its middle-class, upper-class segments) could potentially do better than today.

The worst scenario is one of recession + inflation (i.e. high-rates) like the one Brazil experimented in 2014-2018. This is obviously hard to predict but is a possibility.

To answer what will happen with credit conditions, we can think of scenarios for each of the funding sources we considered above.

Starting with FGTS/MCMV, one could argue that, with Brazil’s unemployment rate at record lows, there is simply no place to go but down, because there are no new workers. However, there are two forms in which FGTS funding can continue expanding:

Salary growth on nominal terms, because the employer deposits are tied to the salary.

Increase in registered workers, because unregistered workers do not contribute to FGTS. Out of the 100+ million workers above, recent studies find that up to 40 million do not contribute to Social Security (IBRE). Further, registered workers have been growing above unregistered workers for this whole cycle (IPEA).

Therefore, the FGTS/MCMV system can continue growing even with a flat occupied population.

This year, the perspective is for credit to continue growing, ~10%, but this is heavily driven by the election year. Policies tending to higher credit include the funding approved for MCMV, allowing Caixa to relax LTV standards, and reforming the SBPE system.

Going forward, the government plans have approved a stable funding level for MCMV from the FGTS into 2029, but obviously, these plans can change with the economy and with a new government.

Another key question, even with a Lula victory in 2026, is whether the government will decide to cool the economy a little in 2027/28, in the first years of the new government, when political capital is high.

Of course, the largest risk is an increase in formal unemployment coming from a recession. Previewing the length and degree of such a recession is kind of futile.

Where I stand in terms of risk/reward is a position of neutrality to slight negativity. We are obviously not at a cyclical bottom with record unemployment, and the best scenario is one of stable growth, not explosive growth as we saw so far. The risk of a prolonged recession is hard to predict but very real, and a new government (even if the same president or party) will probably have the political capital to cool the economy a little.

The remaining credit market of SBPE/SFH and CRI/SFI depends more on credit conditions. Employment is also important but only as a factor in credit conditions, like SELIC or credit apettite.

The best scenario is one of lower rates, where poupança is more attractive, and livre financing costs are lower, but which is not caused by a recession.

In the mid-scenario of higher unemployment but lower rates, we could have a K-shaped market, where the middle and upper classes can access credit because their creditworthiness is not affected and banks look for relatively less risky investments, therefore making funds are more available. In fact, this is what happened in 2017-2021, with SFH/SFI being the driving force of the market expansion from a recessive period.

The 2014-2018 double-whammy

The worst scenario is, of course, an inflationary (high-rate) recession, which is what Brazil got in 2014-2018.

At the time, the economy had been growing, but heating (World Bank, World Bank), in part because the BRL was depreciating (USDBRL went from R$1.5 in September 2011 to R$4 in September 2015). The Central Bank started hiking in 2012, going from ~7.5% to 10% in 2014 (SELIC historicals).

By 2014, the economy had already stopped growing, but because the country experienced depreciation and inflation between 2011 and 2016, the CB continued increasing rates into 14% by late 2016. Only then, with 2x the unemployment rate (World Bank), did the Central Bank cut rates, after two years of recession.

Under this scenario, credit concessions to real estate were halved in nominal terms, and probably cut by 70% in real terms from their peak.

Could this scenario repeat? Yes of course, mainly via a capital flight or balance of payments crisis leading to persistent depreciation and inflation. The 2014-2018, however, seems like a complete coctail: commodity prices collapsing, capital flight, political chaos, austerity, inflation, high-rates, etc. It is very hard to predict another crisis like this, but it has to be kept as a possibility, and ask for a return accordingly.

As a side note, an aggravating factor at the time which is not as present today is that, back then, a large part of MCMV came not from FGTS but from the Federal budget (Orcamento Geral da União, OGU below). That budget was cut with the austerity measures implemented in the second half of the Rousseff government and during the Temer and Bolsonaro governments. Today, funding comes almost exclusively from the FGTS.

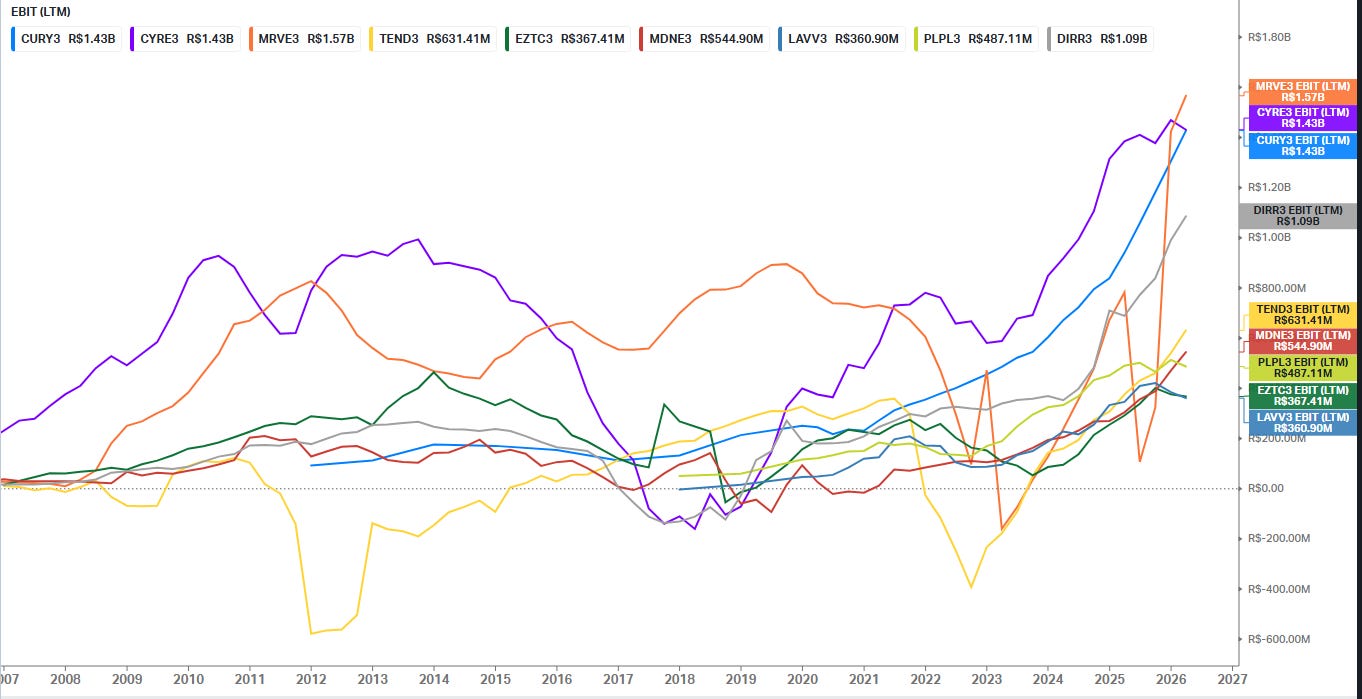

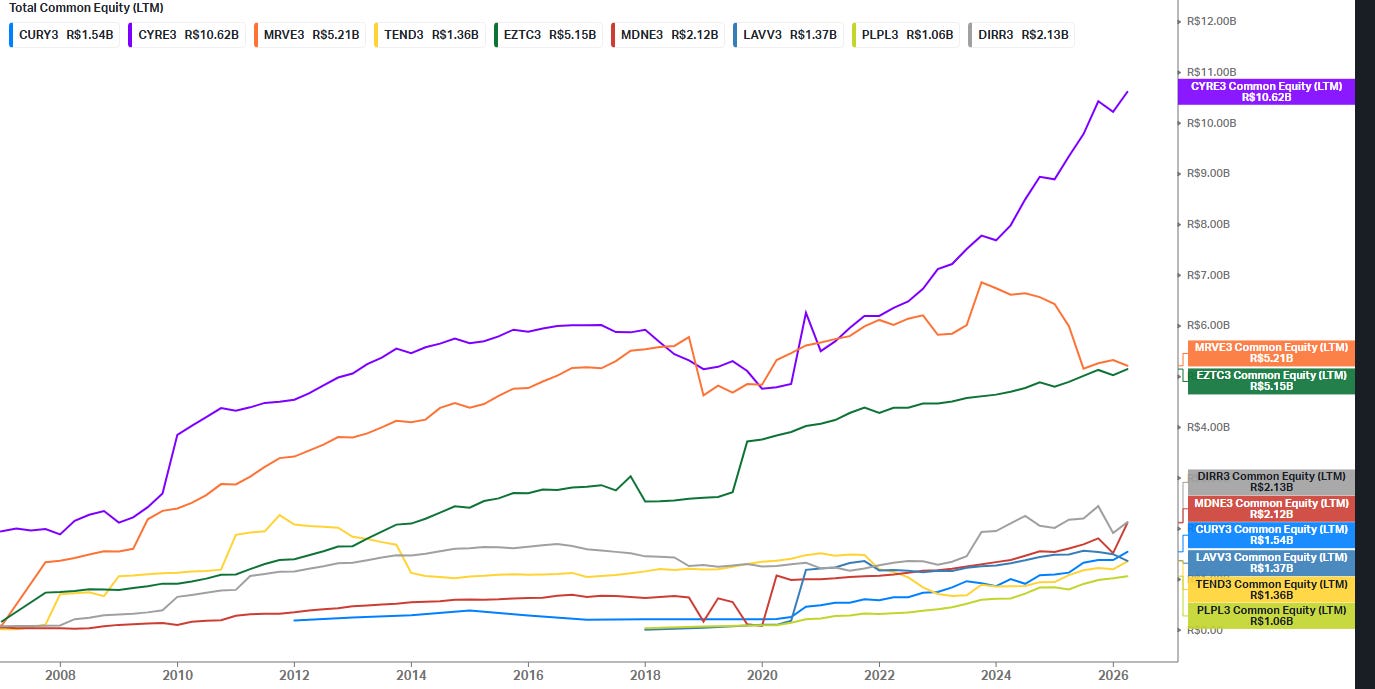

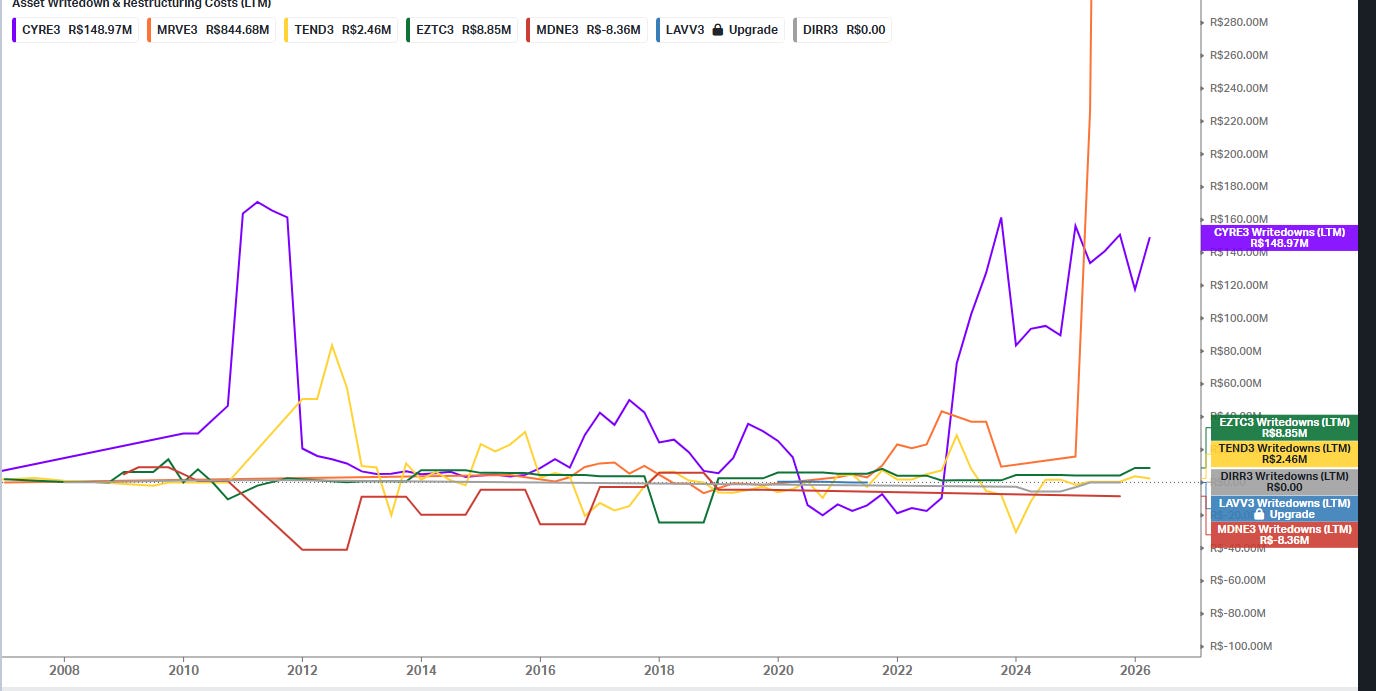

Furthermore, even during the 2014-2018 period, though their operations shrank significantly, the currently public companies remained EBIT profitable, and did not suffer significant impairments or equity challenges.

Valuation models

Of course, I cannot know what will happen with the economy, but luckily, I don’t really need to. We can compare each company’s market cap today (or at some point in the future when revisiting) with estimates of fair value based on operations under different scenarios.

This section includes models for analyzing financial stress (key for real estate developers), NAV, and operating leverage at different construction levels, along with commentary about company-specific factors like segment exposures, balance sheet structuring, and historical analysis.