Alpargatas - $ALPA4.SA

Is Havaianas Coca Cola for the feet?

Alpargatas is a historic footwear manufacturing company (oldest company still traded in the Brazilian exchange), with a rich history in Brazil and Argentina, creating category-defining brands in both countries. Like any old company, its portfolio has changed a lot over the years.

Today, Alpargatas’ only relevant asset is Havaianas, the largest flip-flop brand in Brazil, and, one could argue, maybe globally.

Within Brazil, Havaianas sells 200+ million pairs per year (almost exclusively flip-flops). This implies a 65%+ market share in the flip-flop category, and a 50%+ share within the wider sandal+slipper category.

Havainas sells 1 in every 4 pieces of footwear in the whole country! It’s branded-staple quality renders it similar to Coca-Cola: a product that carries the strongest psychological effects of brand power and yet is within the reach of anyone.

Outside of Brazil, Havaianas sells another 20 million pairs, which is a drop in the bucket of the global market (maybe as large as a couple billion pairs). However, Havaianas’ positioning outside of Brazil could eventually allow it to become a silhouette brand. Similar examples include Birkenstock, UGG, or Crocs. That is, internationally, Havaianas always holds the potential for very interesting convexity.

The business today has recovered from a deep downturn after the pandemic (classic inventory glut). It combines what I believe is a branded-staple product in Brazil that has a good ability to generate relatively stable earnings, with the potential of expanding that brand power to a massive category outside of Brazil.

This article covers the company in detail, including positioning in each market and segment, financial analysis, operational leverage models, taxes, management quality, capital returns, etc.

Vamos lá!

Eu dou amor e o povo me machuca

Meu coração tá igual havaianas, todo mundo usa

I give love but the people steps on me

My heart is like Havaianas, everybody uses it

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. I may own or later purchase some of the stocks mentioned in this article.

TLDR

Havaianas in Brazil is a business that combines staple volumes with branding power and the potential to expand margins via trade-up during good consumer periods. The business showed resilient volumes and margins in 2014-2018. During the post-pandemic glut, it suffered more but still turned a profit. Clearly, among the most valuable consumer brands in the country

Havaianas International offers the potential for growth, but so far, this has proven hard to execute. The business will require significant recurrent investment (and therefore low profits), but the potential is huge.

Capital returns are high (15% NOPAT/Operational Assets). Unfortunately, the capital returns cannot be leveraged, and there’s not a lot of space to put capital to work. Has a strong history of dividend payments.

The valuation today seems a little dear or “quality-like” for Brazilian standards, based on what I believe is a more recurring earnings level. This seems justified by the quality of the brand/business, and is below historical standards, but it’s hard to think of high returns from these prices, unless one is rather optimistic about Brazil or abroad, or expects further multiple expansion.

Still, it is at the top of my list for a Brazilian downturn.

Index

Brazilian market - Chinelos e feijão

Intro and history

Staple segment

Differentiated segment

Estimating volume and sales by channel and segment

Going forward

International market - Cost of growth

Other businesses

Financing and capital requirements

Taxation

Post-pandemic operations

Management quality

Models and scenarios

Past and present consumer cycles

Operating leverage model in Brazil

International scenarios

Capital returns and valuation

Brazilian market - Chinelos e feijao

Brazil represents 90% of the volume, 75% of the revenues, and 95% of the EBITDA of the brand today. It is the heart of the brand.

Sandals are the dominant footwear category in Brazil (380 million pairs, or 45% of the market). This makes a lot of sense, being a tropical country (blessed by God and beautiful by nature, we should add). Dominating the largest market, Havaianas is the largest footwear seller in Brazil (~25% of the whole market).

I don’t think any other global footwear brand can claim 25% market share of a large country, across all categories. The brand sells, on average, one pair to each Brazilian per year.

This moves Havaianas from footwear to a form of staple product, with some volatility given by the cycle, but overall, fairly stable characteristics, particularly around volumes.

Havaianas was created in the 1960s and for its first 25 years it was primarily the footwear of the people. During the 1980s inflation crisis, the government put Havainas in the controlled price list. However, its original popularity, low price, and simplicity, had converted it in a form of inferior good.

Then, in the early 1990s, Alpargatas decided to elevate the brand via massive marketing campaigns, generally starring personalities from Brazil and transmitting a feel-good attitude (the most recent example has Vinicius Jr, Brazil’s most relevant football player today). The core slogan became ‘Todo mundo usa’ (Everybody uses it).

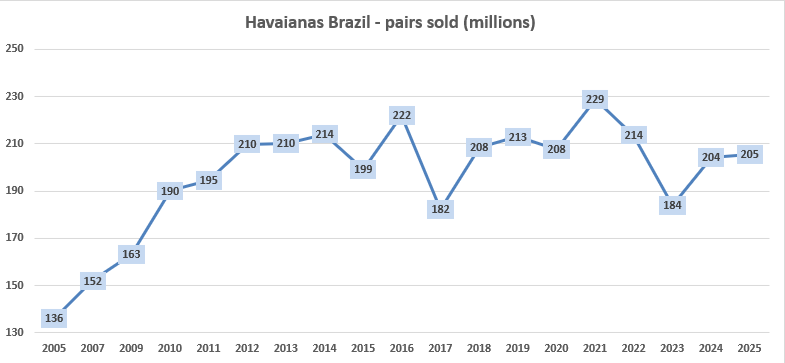

The brand grew like wildfire in the 1990s and 2000s: in 1993 it reached 100 million pairs, by 2005 it had grown to 136 million pairs, and then added another 70 million pairs in the next 7 years.

However, the brand has been unable to surpass the heights reached at the peak of the Brazilian boom in 2012/14.

Even though it has not represented growth, the brand’s volumes have been extremely resilient to severe crises in Brazil (2014-2019, 2021/23). The volatility of volumes seems more related to channel stuffing/destuffing than to end-demand, which seems fairly stable at ~205/210 million pairs per year.

Staple segment

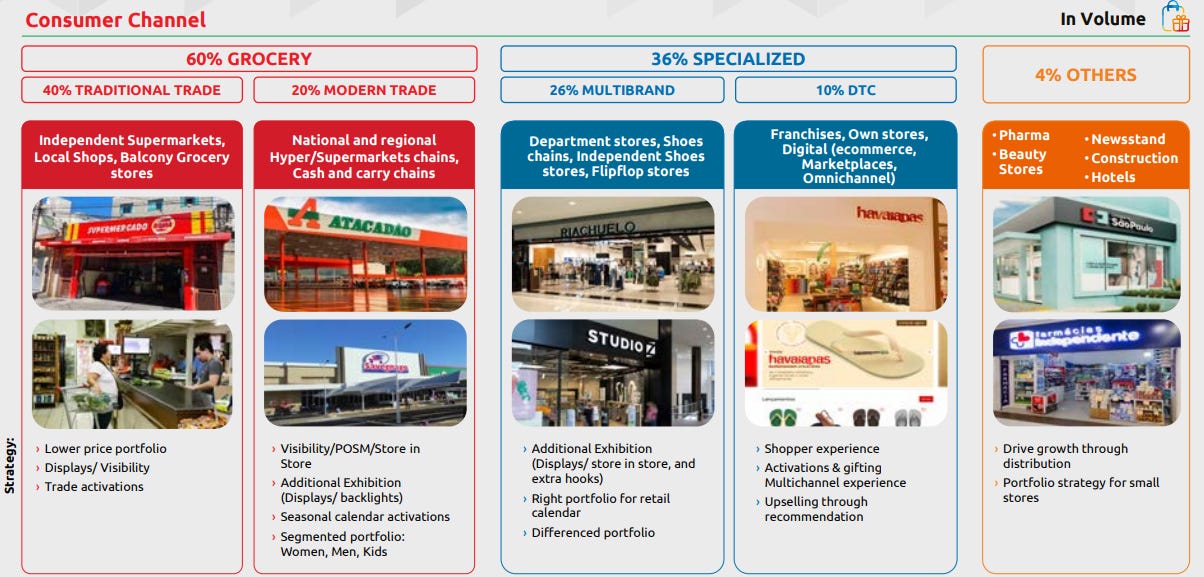

Havaianas' stapleness is evident in its price and in its distribution channels. The cheapest pairs can retail for R$25/30 ($5 each), and 65% of the brand’s volume is sold in grocery stores, supermarkets, and pharmacies.

40% of the volume, skewed towards the cheapest options, is sold in local, small-scale groceries. You go and grab some rice, some feijao, and a pair of Havaianas. For stores, the Havaianas is a high-impulse but recurring sale, usually in the hot area of the store (example). This market is served by a network of also relatively small distributors and resellers (example, example, example).

The distribution in this particular channel (small-scale grocery, where the company claims a whopping 87% share) is probably a particular challenge and a source of moat. Whereas rice is the same for all customers, stocking sandals is a different game altogether because there are quite a few more SKUs (sizes to begin with, but also colors and styles). This is a long chain. The small store buys from a reseller in the commercial district of the city, who then buys from a larger distributor, and so on. It is also probably a source of volume volatility, in the form of the inventory bullwhip effect.

Differentiated segment

As mentioned above, Havaianas is not only a staple brand, but has also tried to capture higher-differentiation segments above the cheaper options.

Today, one can find a variation of the classic silhouette at R$140, or variations of the silhouette for R$250+. In the traditional footwear channel, like shoe stores and apparel stores, the majority of sales belong to these upper-price categories.

Estimating volume and sales by channel and segment

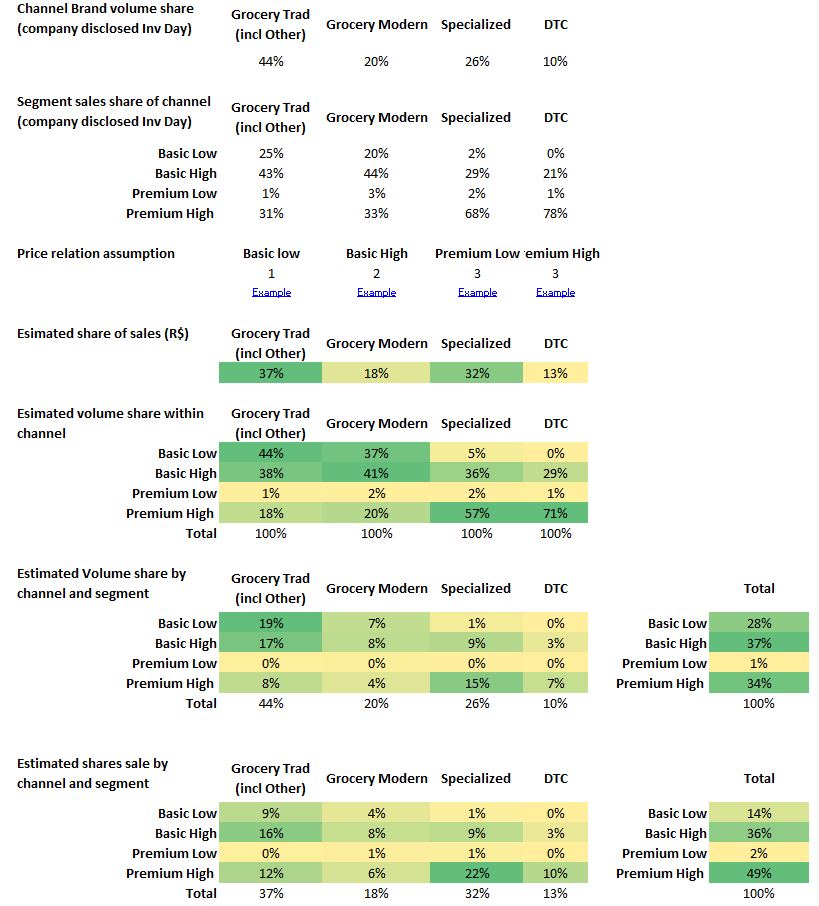

The company only reported in its Investor Day the volumes by channel, and the sales percentage by segment and channel.

However, based on only two sets of assumptions, we can estimate/speculate around the aggregate volumes and sales by segment, channel, and combination.

The two assumptions are:

The sales price across channels is the same for a specific price segment. That is, the company sells a basic product for say R$5 to Grocery Trad and to Grocery Modern or DTC. This is not true (the longer the chain, the lower the sales price, so one piece sold to Grocery Trad probably represents less revenue than if sold to Specialized or via DTC), but I haven’t found any info on which to work around it.

The price relation between the segments, which I estimated as 1x for Basic Low, 2x for Basic High, and 3x for both Premiums (Premium Low is irrelevant). Again, someone might question this, but it is what I found most reasonable.

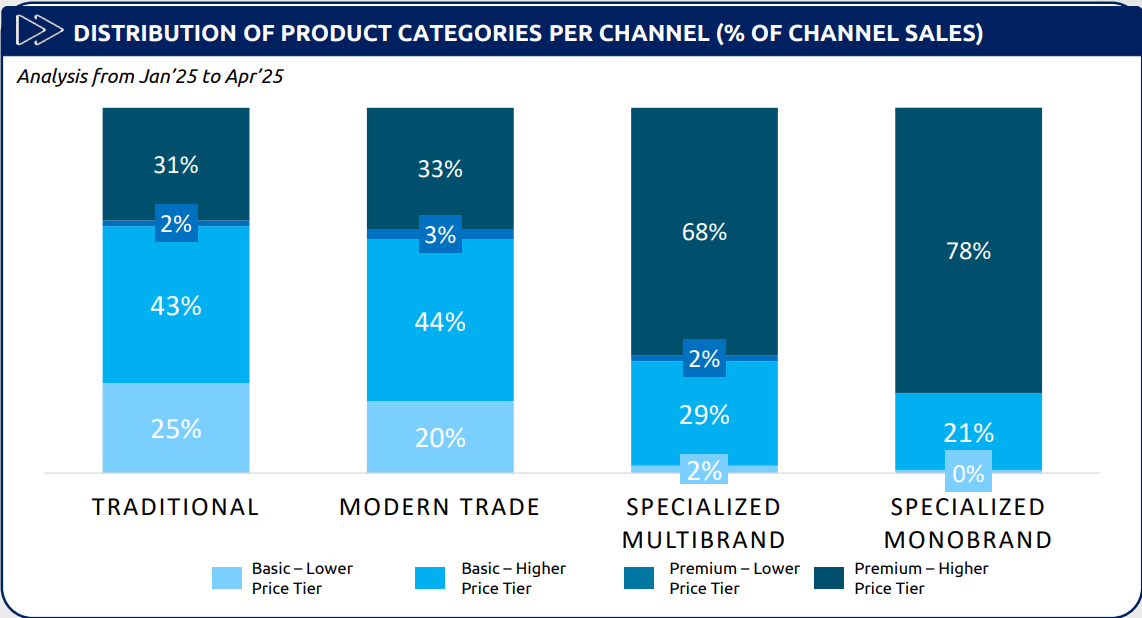

What we find is quite interesting:

The sales share of the channels is similar to their volume share, with a little underweight in Grocery (more cheap products) and overweight to Specialized (more expensive products).

Overall, though, the 55/45% rate between grocery and specialized+DTC is maintained as a percentage of sales.

This makes sense given that the grocery businesses still sell a relatively premiurized product (30% of sales are premium models, 40%+ are upper basic).

The highly protected (in my opinion) traditional grocery business still retains a high percentage of sales, similar to volumes.The basic models make up 65% of volumes and 50% of sales across all channels. Interestingly, premium models make up 50% of sales and 1/3 of volumes, and the upper basic models make up anothet 35% of sales and 1/3 of volumes. This strikes me as a high level of premiumization. This is even true of grocery trade, where premium models are 30%+ of sales, and 1/5 of volumes.

Moving forward, I do not see significant challenges or opportunities in the Brazilian market, but rather a profitable and defensible market. The brand has to defend its position from its own mistakes, especially by not milking the cash cow excessively to the point of alienating lower price points or disinvesting in marketing.