How the search for markets for a post-gasoline world disrupts the olefins cycle.

∙ Paid

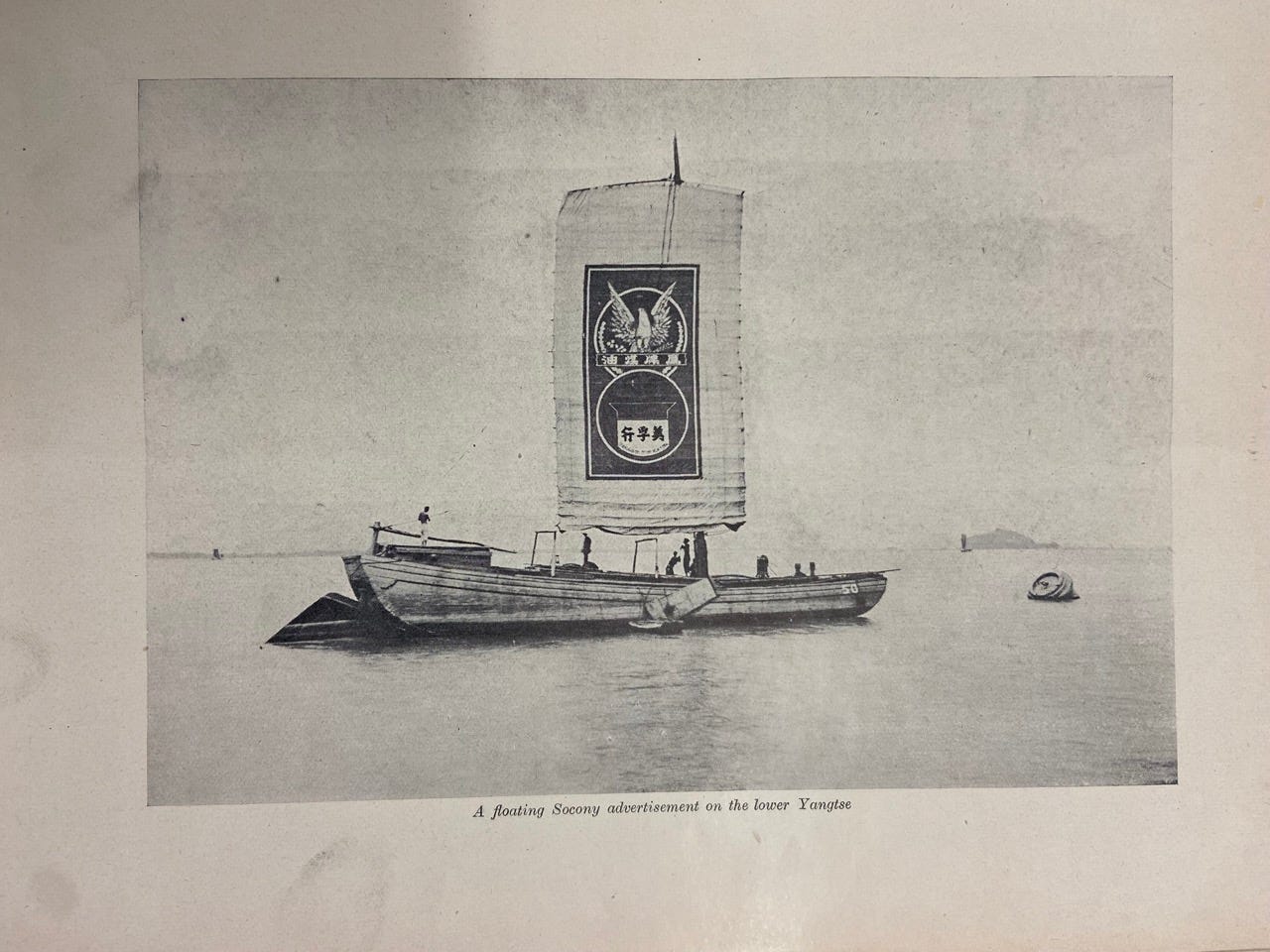

A boat advertises the Meifu kerosene lamps (美孚灯) sold as a loss-leader by Standard Oil (SOCONY) in China, in order to then market kerosene - Image from ModernisModernity

The Chemical industry is under…

Continue reading this post for free, courtesy of Quipus Capital.