[free] Brazil Fast Fashion Overview

LREN3, CEAB3, RIAA3

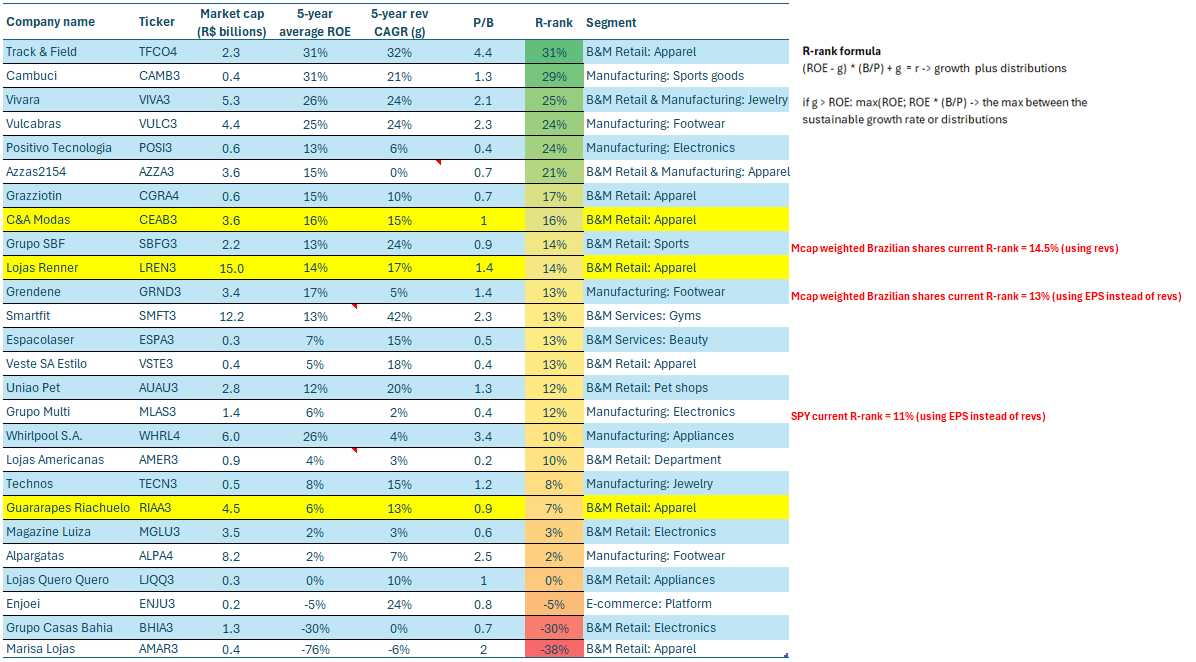

In my last post, I screened and skimmed over Brazilian consumer discretionary names.

Among these, two of the three fast-fashion retailers in the country came up in the upper half of the table, with an R-rank close to 15%.

These businesses enjoy some branding power (they probably represent around 25% of registered Brazilian apparel retail), and have some moat in the form of a fast-spinning vertically integrated structure from design to DTC.

No global fast-fashion retailer (Zara, H&M, Uniqlo, etc.) has a relevant physical foothold in Brazil.

Further, before the pandemic, these businesses used to generate 15%+ (even 25%+) returns on equity, and grew revenues quite fast, even though Brazil went through a challenging recession in the 2014-2019 period.

Because of these factors, I thought these names deserved at least an exploratory review.

What I found is that the recent capital return challenges can be adscribed more to capital allocation than to a market deterioration. On the contrary, these players seem to have maintained share and margins against impacts such as a not so spectacular economy and against the Chinese cross-border competitors (Shein). Knowing this, their future capital allocation will greatly determine returns, even more than where the economy goes from here.

TLDR

Short model and business intro

Fast-fashion doesn’t really need much intro: Zara, H&M, Uniqlo are global players. The core of the model is to integrate a vast B&M network with fast design-sourcing-distribution loops. Brand identity is focused on price/quality positioning for a wide population segment, with just a little of design/style identity. In the best scenarios, the model enjoys the margin benefits of branding without the fashion-cycle risk of identity-heavy brands.

In Brazil, fast-fashion is domestic: Renner, Riachuelo and C&A are the largest players. The foreigners never managed to set foot, with Forever21 leaving, and Zara and H&M having moderate operations (~50 stores between the two). The three local players account for 20/25% of the registered apparel retail market.

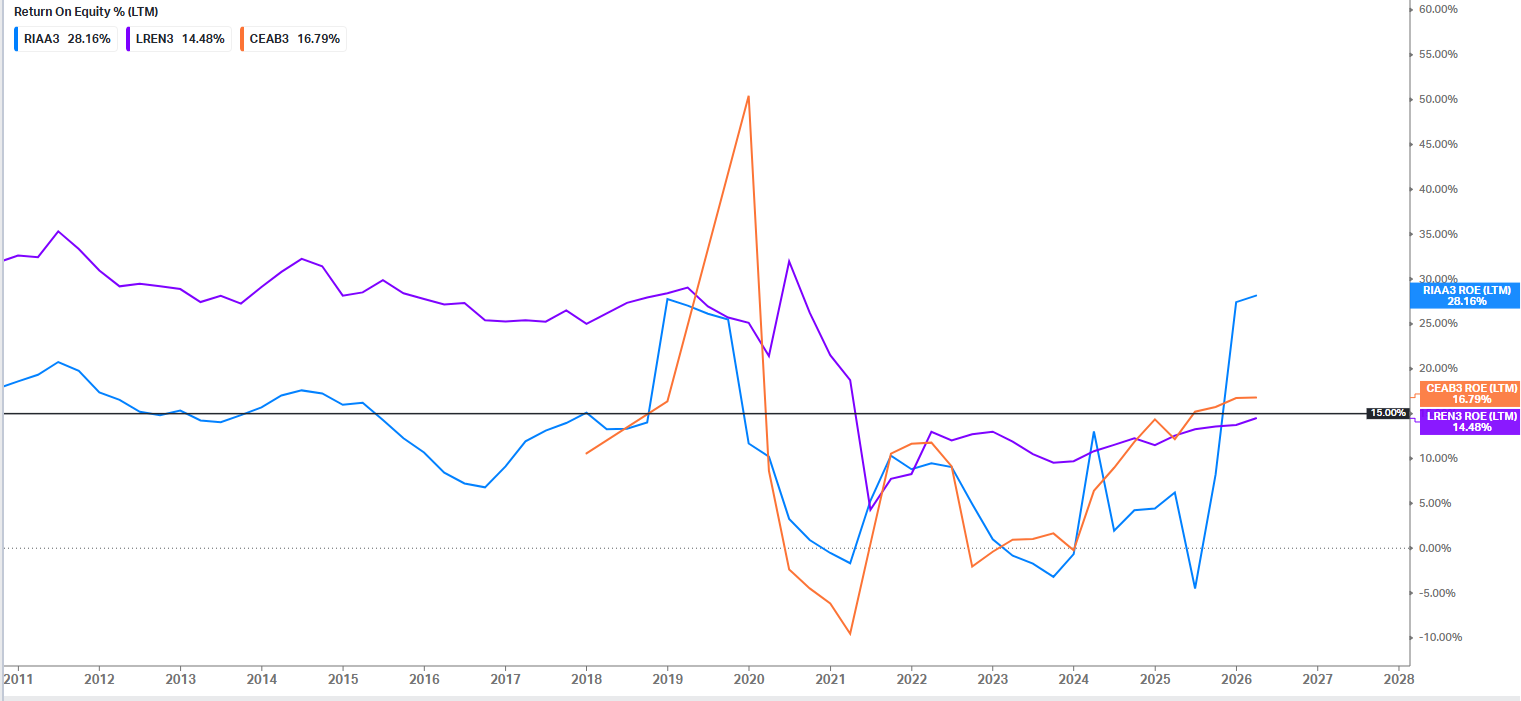

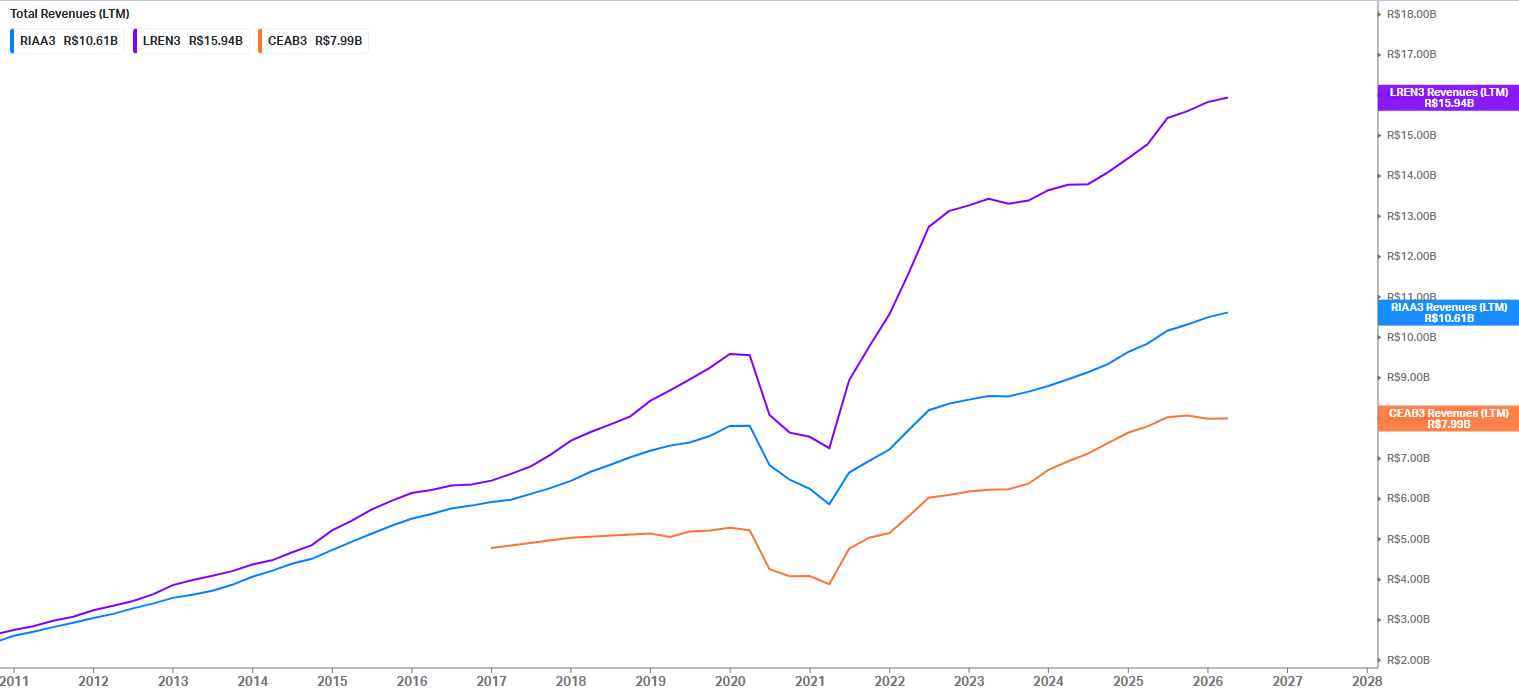

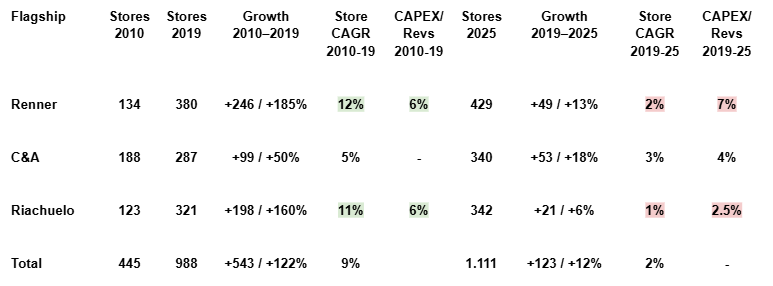

Of the three, the most successful historically is Renner (LREN3), now a fallen angel. The company grew revenues by 10x between 2006 and 2019, while keeping ROEs above 25%. The stock did a 30x during that same period. Renner’s historical CEO, José Galló, is a management legend in the country. Today, Renner’s returns on capital are lower, and growth has slowed quite a bit in real terms, but it remains the largest player, with ~800 stores and R$15 billion in revenue (10% of the registered market), and the one with the highest margins and capital returns. Besides the flagship Renner, the company also has a younger-consumer brand (Youcom) and a house decor brand (Camicado).

Following in size is Riachuelo (RIAA3), at about 450 stores and R$10 billion in revenues. The company grew at a similar pace as Renner up to the pandemic, but at consistently worse capital returns. In part, this might come from having its own production base in the country’s northeast.

Finally, we have C&A (CEAB3), which has a shorter public history (IPOed in 2019), but has been another historical player since the 1980s and 1990s. Today, it is the smallest in terms of revenues and stores (~350).

Little differentiation

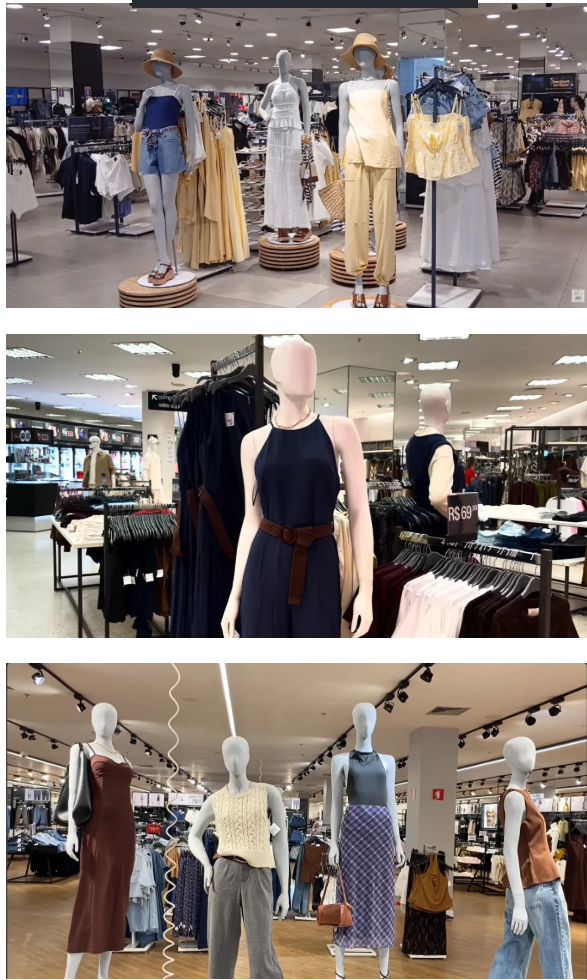

Outside of the historical factors benefitting Renner and their current relative size, the three companies are very hard to differentiate.

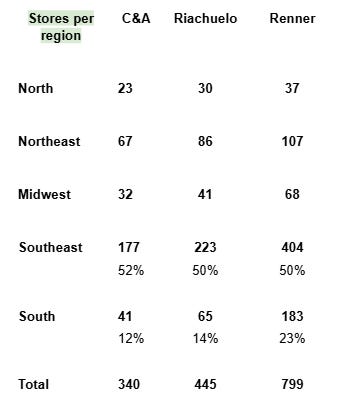

All three target primarily a middle-class 30-year-old female consumer. As seen below, their stores are basically indistinguishable; they all focus on the country’s Southeast/South, and have a similar pricing strategy.

{kind=link}

Why did returns go down in the post-pandemic?

A key question I have tried to answer about these retailers is why the post-pandemic returns have been so much lower than in the 2010s-2020s, and whether they can improve.

I have found a few potential explanations.

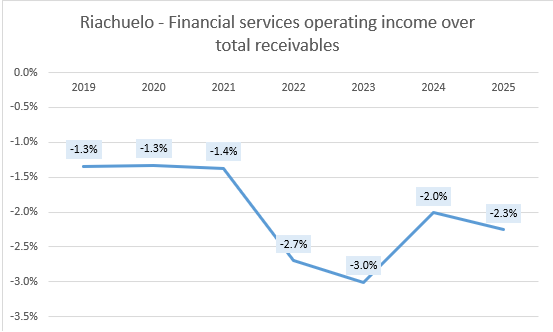

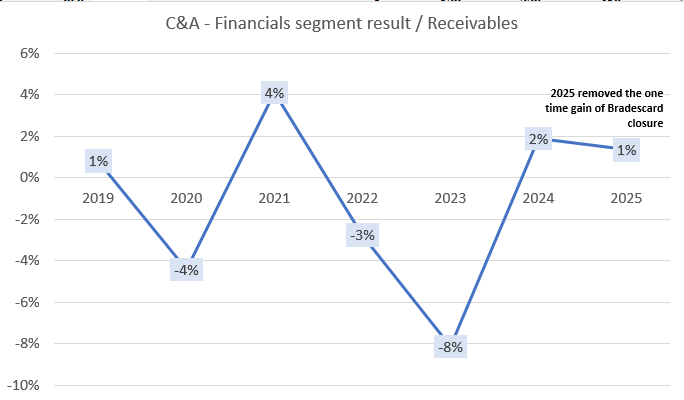

Losses in financial services

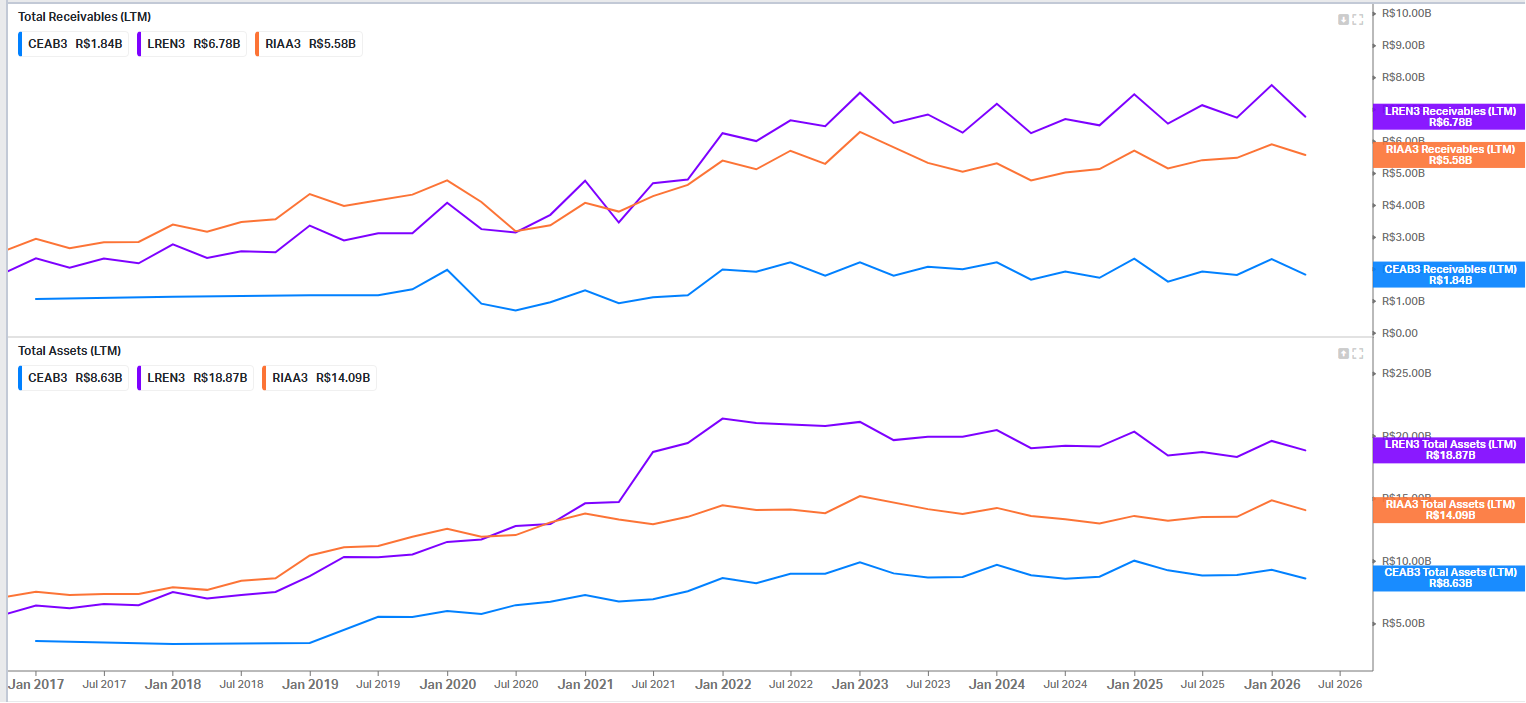

All three retailers have large financial services arms that lend to their customers via co-branded credit cards, installment plans, etc. These lead to high levels of receivables for what could be expected from a retailer (between 25% and 35% of all assets). C&A levels are lower because, until recently, it carried its installment program in a partnership with Bradesco.

The retailers carry these operations within operating income, leading to these having an important impact on capital return figures.

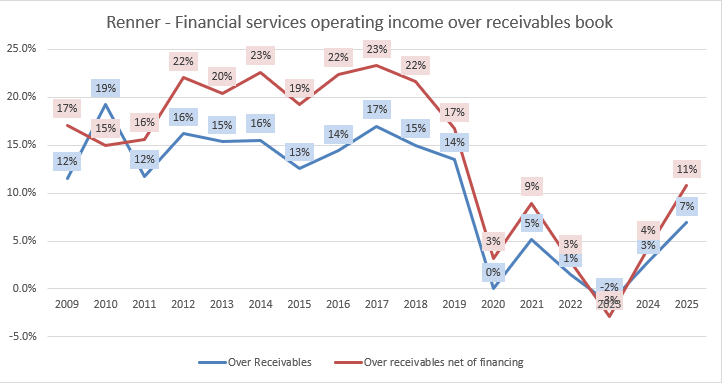

In the case of Renner, the returns on these receivables collapsed as the company expanded co-branded services (adding non-retail-related credit risk), and then suffered from high NPLs as rates increased in 2021/22.

Riachuelo and C&A have not even been able to generate positive income from this segment, which represents 30% and 20% of assets.

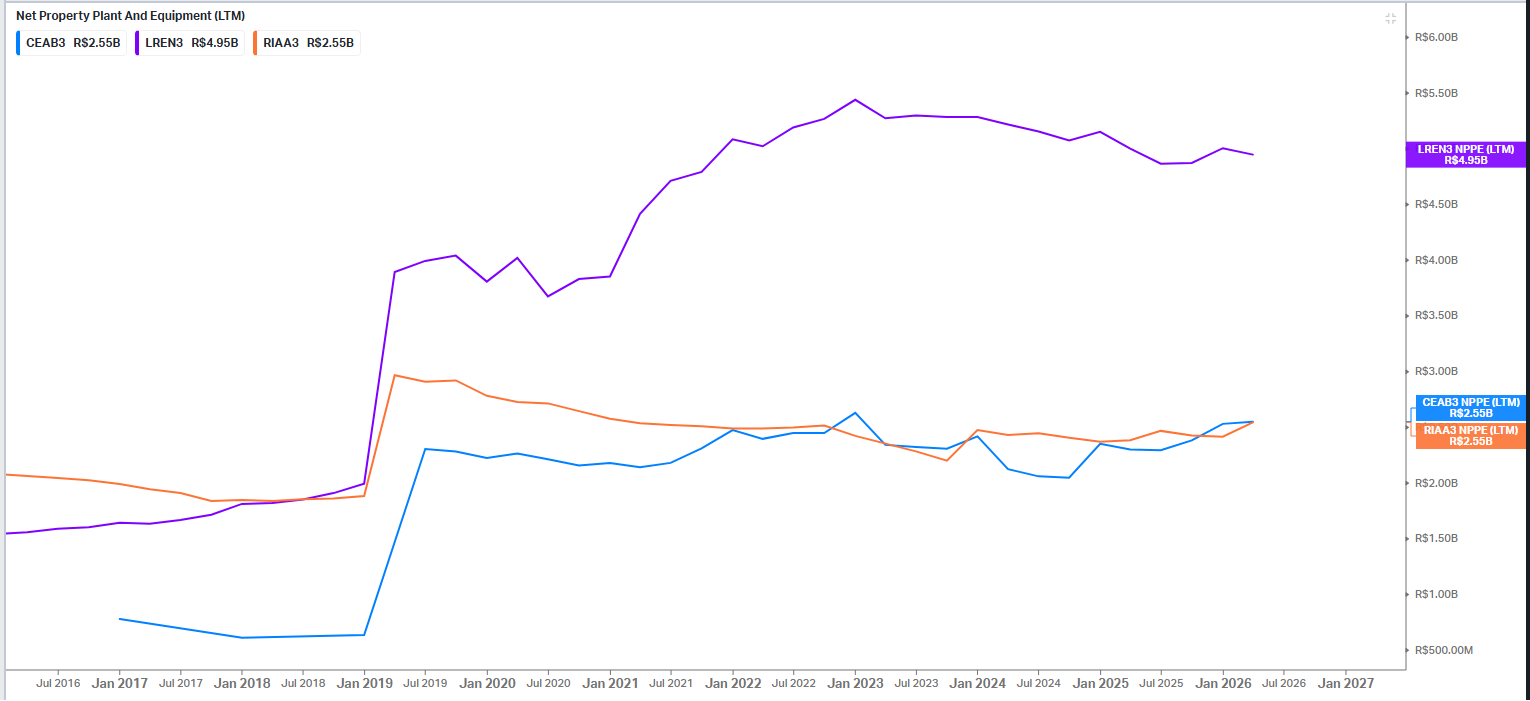

Lease accounting

In 2019, all three retailers implemented IFRS-16, which mandated adding leases to the balance sheet as an asset (Right of Use) and liability (leases). Although this shift also increased operating income because it shifted some lease expenses to financial expenses, it still had a negative effect on asset turnover and returns on assets.

Still, by definition, this should have been neutral on returns on equity.

Format saturation & investment ‘sinks’

There are so many places where you can put a large 2000 square meter store as these retailers have, specially when the ideal location is an upper middle class shoppign mall.

Brazil is large, but may not be THAT large. Having no more space to grow, they may start competing with each other, or reaching out to less valuable areas.

Potentially because of this, plus the added impact of the pandemic digitalization boom, the three invested heavily in technologies such as automated distribution centers, RFID, DTC capabilities, totem checkouts, etc., which did not increment productivity in a similar fashion. Below when comparing store growth vs CAPEX/Revs, we can clearly observe how CAPEX intensity did not decrease in a way commensurate to the deceleration in store expansion.

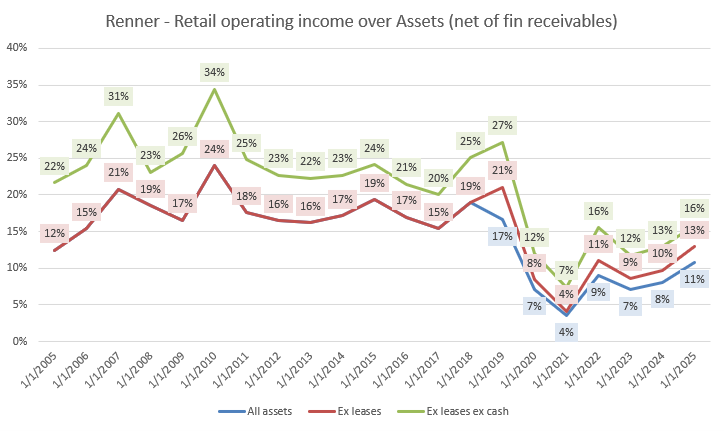

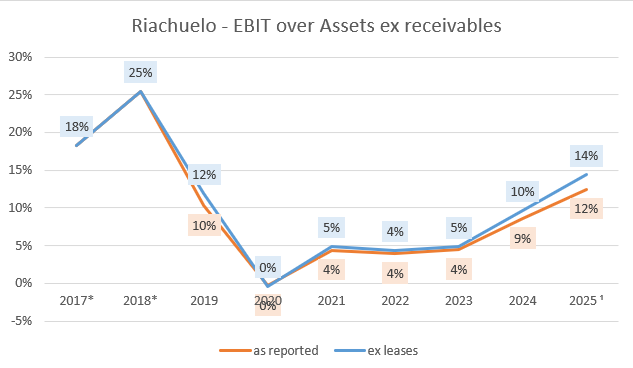

In the case of both Renner and Riachuelo, we can see that even removing the financing operation (receivables) and leases (and in the case of Renner, cash to account for an equity raise in 2021), returns on assets have decreased in the post-pandemic period.

Puting Renner as an example, outside of receivables and ROU, the company expanded PP&E, intangibles, and inventories by R$2.3 billion or 56%. This is in line with inflation (around 50/55%) and with sales in retail (~60/65%), but at the same time, operating income in retail only expanded by 4%.

Forward expectations

The past is informative, but what matters are views about the future. Specifically, what can happen with each component of earnings and distributions.

Retail margins and discretionary exposure

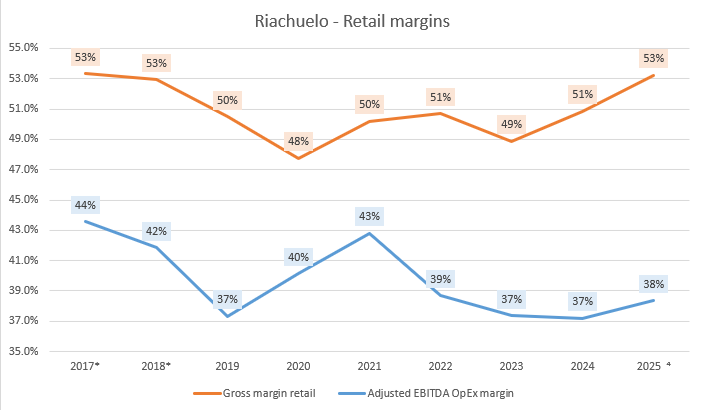

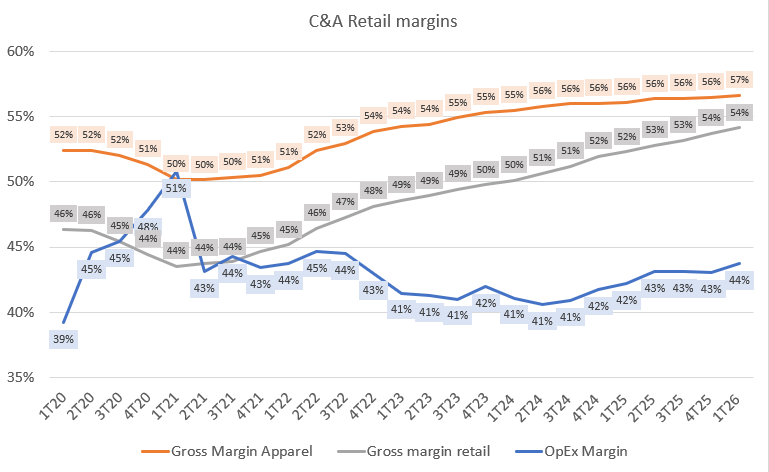

Interestingly, as seen below, except for the period between 2020 and 2022, the margins in apparel retailing (excluding the financial services arms of the players) have actually expanded for C&A and Riachuelo.

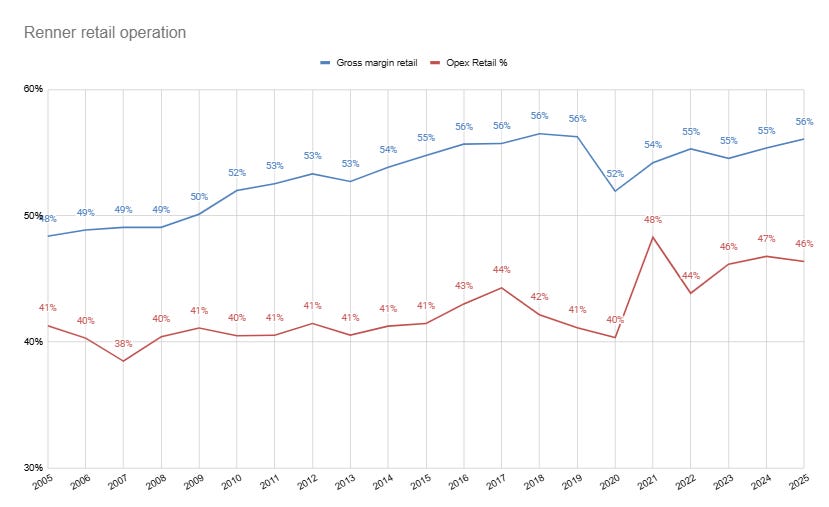

Renner has lost about 4pp of margin during that same period, entirely on OpEx. This is interesting because, being the largest player and the one with the highest original gross margin, one would have expected gross margin pressure, not OpEx pressure. This might indicate execution/control problems. The loss of margin is even worse when we consider that the lease accounting reform actually sends part of OpEx to financial expenses. When adjusting for this, the OpEx-driven loss of margins may have reached 6pp.

The three businesses have also coalesced into a similar margin structure, with gross margins in the 55% region, and operating margins in the 10% region.

Overall, though, I think this speaks of some degree of margin durability, at least on the gross margin side (the consumer facing side, in some sense). This is a relevant read because 2020-2026 was not an easy period for apparel retailing.

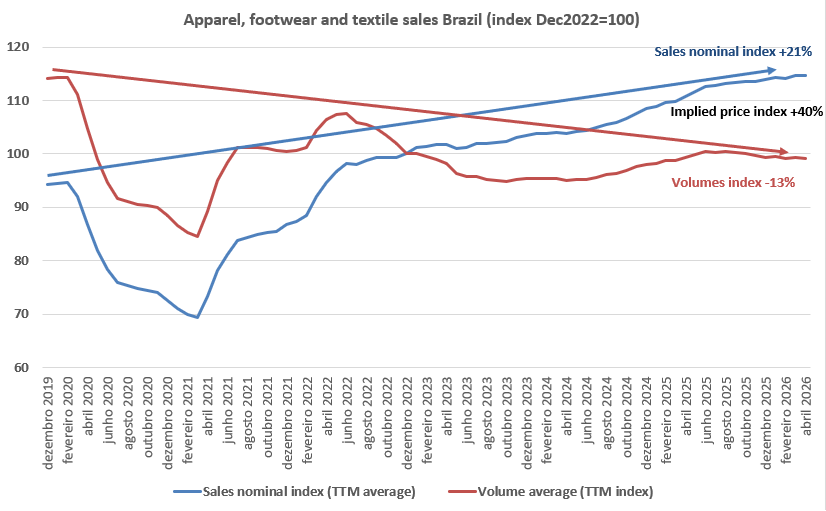

On the one hand, we can observe below that at the national level, apparel volumes were down when compared to the pre-pandemic period. Prices, which rose 40%, were below inflation (55%). So this was not a booming period for apparel nationally.

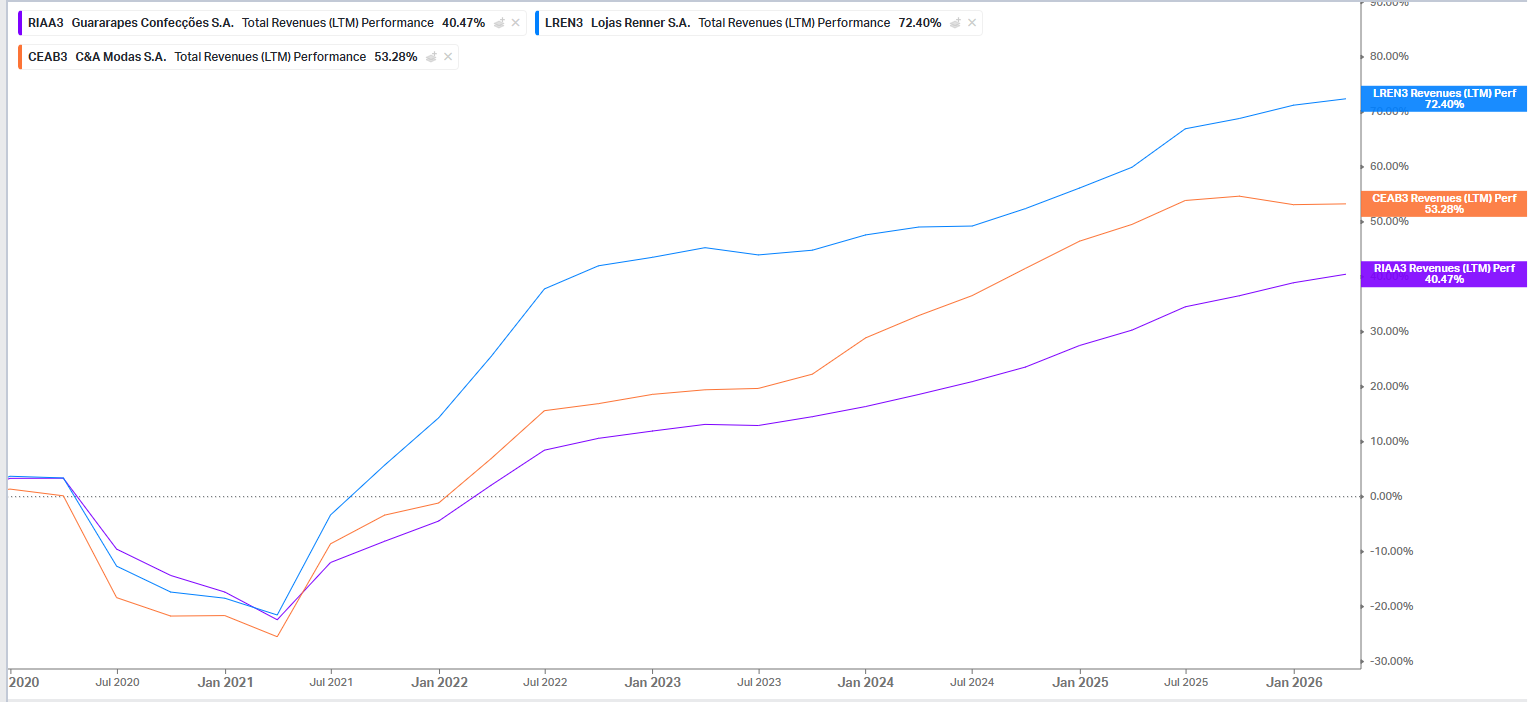

In such a context, all the local players grew above the sector and did not lose (but actually gained in C&A’s case) gross margins.

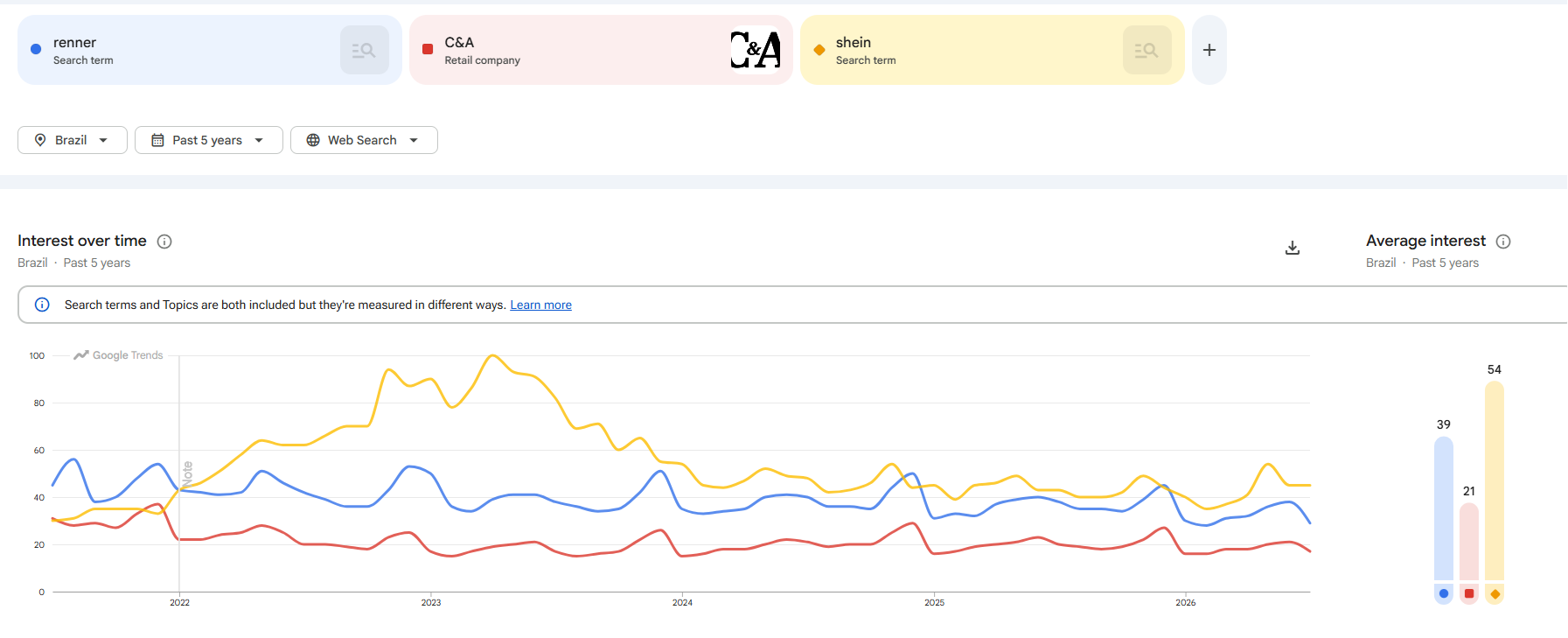

Further, we had the impact of Chinese cross-border e-commerce (Shein, Temu, Shopee). Depending on estimates, these platforms could have gained up to 10% of the apparel market in Brazil. A 20% tax (called Blouse Tax because it was specifically focused on Shein) was enacted in 2024 and helped repel this competition, but the tax was derogated in mid 2026.

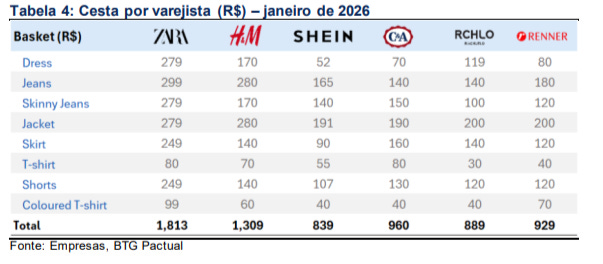

If we refer to the BTG price calcs below, before the repeal of the tax, Shein did not show a massive price difference with the local players.

That is, the retailers were able to compete (with some tax help that is now removed) with the Chinese cross-border players, without much margin impact. Further, it is interesting to see that after a boom in the post-pandemic, Shein’s search interest in Brazil is very close to that of Renner or C&A.

This all leads me to believe that the retailer’s model is more defensible than what one would expect of undifferentiated apparel retailers. Despite a challenging economy and new aggressive competition from abroad, they were able to grow above inflation, above their sectors, and expand margins (except for Renner).

Finally, a topic to have in mind in the next few quarters is the impact the 5-day workweek will have on labor costs for the retailers. This could easily become a source of problems as S&M (personnel line) climbs.

Financial segments kept in line

Given the impact the financial arms of the retailers have on capital returns, it is relevant to review each of the company’s plans. Only Renner has a profitable financial operation, generating around 25% of the company’s operating income.

Capital allocation

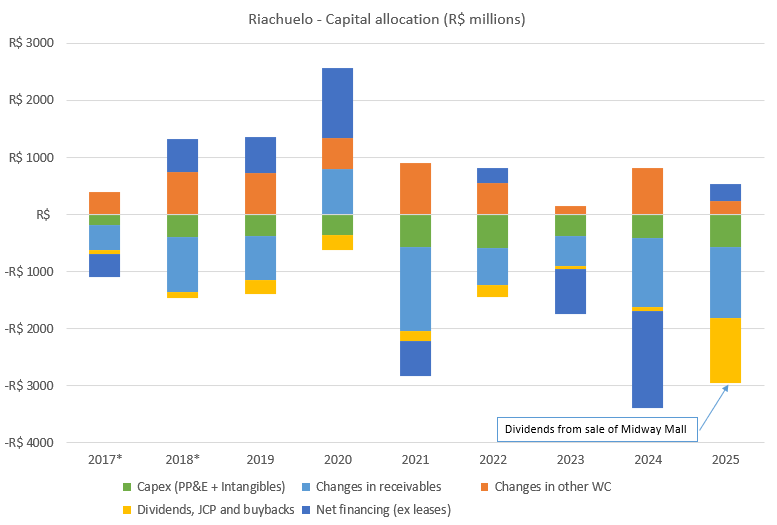

Finally, we have Riachuelo, which has invested more aggressively in its receivables program and in deleveraging post-2021.

The company’s distributions have been scant, except for specific dividends from the sale of the Midway Mall.

The company is expecting to reinvest capital, given that it has expansion plans, and had intended to raise equity as early as March 2026.

Scenarios and investment return analysis

All of the above is nice information, but it is not very useful without considering the potential analysis of returns under two scenarios (the current discretionary context and a more pressured one).

Conclusions

Three things call my attention about the fast-fashion apparel retailers after studying them in more detail:

Their models have coalesced in terms of price, store, and margins. They have differing margin dynamics today, but I speculate that this cannot last when the models are so similar.

None of the three strikes me as improving businesses in terms of growth space or margin space.

This is why what ends up really differentiating the return dynamics is capital allocation. Renner, which has a worse margin dynamic, ends up above C&A and Riachuelo because of where it wants to spend capital (primarily distributions, then some store growth).