Forest Industries I: Basics

The Forest Industries are a long value chain, extending from natural and planted forests through processed wood materials vital for construction and furniture, and through pulps that become everyday paper and packaging.

The cycles of the Forest Industries are driven by geographical and economic factors like availability and cost of raw materials, through capital and processing capacity, and finally end-demand drivers, like construction, e-commerce, or CPG retailing. Some links in the chain compete very locally, while others are global.

In recent years, different links of the value chain across geographies have been under high cost and margin pressure. Common traits of these pressured cycles are high raw material costs and supply shortages, excess capacity buildup, and ailing end-demand.

Like with many other cyclical industries, the end goal of this analysis is to try to find low-cost, underlevered players, trading at attractive multiples of estimated cycle-average earnings.

Given that the majority of the players in the industry span several links of the value chain, this article tries to provide an overview of each link, how it is distributed globally, competitive drivers, and the recent cyclical situation.

This will come in handy when evaluating the companies in future deliveries.

Without further ado, chop chop chop!

Index

A map of the value chain

1. Forestry globally

a - Types of wood and wood qualities

b - Types of forests

c- Productivity of forests

d- Trade

e- Challenges in supply and elasticity

Why not South American softwood?

Oil shortage impacts

2. Wood products

a - Product types and uses

b - Trades

c - Scale

d - Cyclical position

3. Pulp and paper

a - Mini-review of virgin pulp (aka chemical pulp)

b - Recycled pulp

c - Paper types

d Trade

e - Scale and specialization

f - Cyclical position

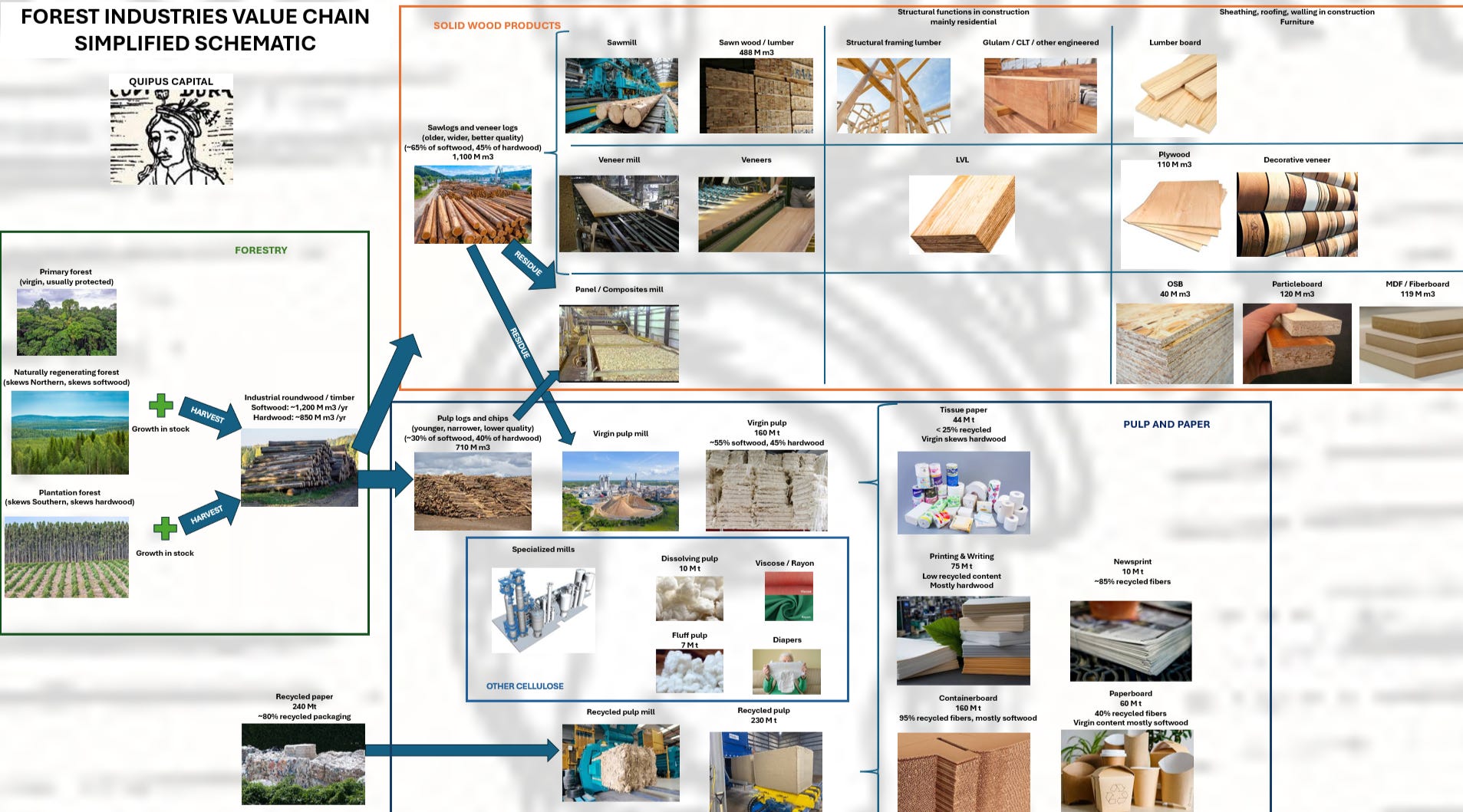

A map of the value chain

The schematic above shows most of the value chain of forest products and the industries reviewed in this article.

As we can see, it includes four main industries:

Forestry: wood obviously comes from trees in forests. Some of those forests are specifically planted for wood harvesting, whereas others are natural forests from which a sustainable level of wood is harvested each year. Forestry is the basis of competitiveness in downstream industries because of the weight of fiber costs in overall product costs, and because 'raw’ wood is expensive to move around.

Wood products: These are what we would usually think of as a wood product, going from a piece of lumber used for structural purposes in construction, to the composite material inside and the veneer covering outside a piece of furniture or cabinetry. The majority of the demand for wood products comes from construction, where wood is used either as a structural product, as a layer, or for decoration. This is especially true for North America and Europe. Wood products have different degrees of ‘value added’ with respect to their original log qualities, from a simply dried and sawn structural lumber piece (usually classified as solid wood products) to a completely manufactured LVL or MDF piece (classified as composite or engineered products).

Pulp and paper: The second big category of products made from wood is paper, including printing papers, tissues, cardboard, and packaging materials. The largest portion of the paper market is packaging, both containerboard used in transportation, and paperboard used for product storage and cutlery. A large percentage of packaging is made from recycled paper. Still, part of packaging, and other uses like tissue or printing paper require virgin pulp as well, which is made from pulplogs coming from the forests.

Finally, we have a category called Other Cellulose, which groups several smaller industries made from pulp (also called cellulose). These include dissolving pulp, which is transformed into the viscose/rayon fabrics; and fluff pulp, which is used as the absorbent agent in diapers and similar products. Not included in the schematic are even more sub-industries derived from cellulose that make chemical products (acetates, carboxymethyl cellulose, microcrystalline cellulose). These are not covered in this article.

1. Forestry globally

Summary

Wood can be classified into two types: softwoods and hardwoods. Contrary to their name, softwoods are used for applications where resistance is desirable, in both solid wood and paper products.

A specific tree can be classified as a sawlog or pulplog. Sawlogs are larger, older, and of higher quality; they can be used for solid wood products. Pulplogs are younger, smaller in diameter, or may be damaged, and can be used for pulp or for composite products. The same tree can be partly converted into a sawlog and partly into a pulplog.

Wood can come from both planted and natural forests (which is not the same as a virgin forest). Planted forests are more common in the Southern Hemisphere for hardwood and pulpwood, and natural forests are more common in the Northern Hemisphere for softwoods and sawlogs. Natural forests are plentiful, but harvesting them is usually a big challenge compared with plantation forests.

A forest’s productivity is measured by two components. One is biological, the amount of wood it grows in a given year (measured in m3/hectare/year). The second, and just as important, is logistical, how easy it is to collect the wood, consolidate it, and transport it to the mills that need it.

Wood in raw form is a very low-value-density product, and therefore, its trade between countries or regions is highly limited. This ends up determining the location of downstream industries that require access to ‘raw’ logs.

Currently, many regions are suffering from supply limitations of forest wood, caused by political (Russian supply to Europe, Canadian regulation) or natural factors (calamities in Central Europe). These supply challenges evidence that wood is a generally highly price-inelastic raw material, where supply does not increase to adjust to demand in a context of higher prices.

The current supply challenges of oil (this article is written at the end of March of 2026) will impact forestry above all.

The forestry industry sits at the basis of competitiveness across the forest products complex. Fiber costs make up a large share of the cost of final products, whether we are talking about pulp, paper, lumber, plywood, or panels. And unlike many other raw materials, forests cannot be relocated, nor is wood particularly easy to transport. Even within the same country, having a forest resource 50km away versus 250km away can be the difference between being globally competitive downstream or not.

In many geographies, supply challenges in forestry are driving a large share of the pressure being felt by downstream forest industries in the form of high delivered wood costs or outright low availability of timber.

This section reviews the basics of the forestry industry, the types of wood and forests harvested, the logistical challenges presented by wood, and how this ends up shaping the location of downstream industries.

_Albertina_DG1926-1779.jpg){kind=link}