Brazilian Meatpackers: Cyclical turn?

2Q26 update of Brazilian meatpackers

The Brazilian meatpackers are a very interesting industry.

One of the clearest examples of multinational giants that call Brazil home and have a relatively strong global position, these companies built global platforms in meat processing based on the competitiveness of the Brazilian soil. Starting with Brazilian cattle, they expanded into other geographies and proteins via acquisitions during cyclical downturns. Today, Brazil ranks first in global beef and chicken exports, and third in pork.

Meatpackers enjoy secular tailwinds, as developed and developing countries alike seem to have an insatiable hunger for protein, a food considered healthier every day.

Because of barriers to entry in export markets, the meatpackers can absorb a large share of Brazil's competitiveness when animal supply is plentiful.

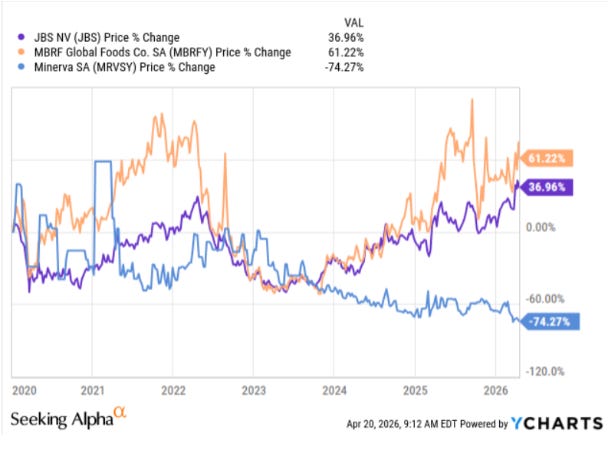

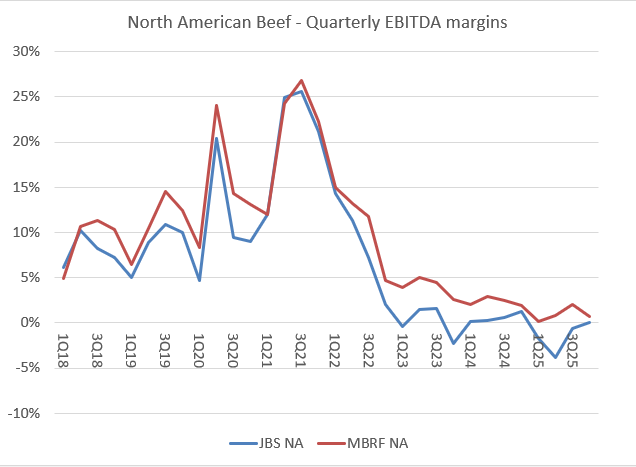

For the past three years, the margins of the meatpackers have expanded thanks to climbing protein prices coupled with stagnant or falling grain prices. The Brazilian cattle herd cycle has been positive for Brazilian exports at the same time as US herds reach minimums. This has helped their stock prices in the cases of JBS and MBRF (Minerva underwent its own leverage and acquisition integration challenges).

However, cycles never last forever. Brazil’s cattle herd is expected to decline, grain prices are climbing because of the Hormuz situation, and Asian markets might be hit by the economic impact of the war and currency depreciation. This situation finds some of these companies pretty levered, and paying BRL interest rates that are above their returns on capital.

In this overview, I revisit previous works on the meatpackers and add analysis for the cycles of the future.

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product.

Index

Meatpacking industry basics

Brazilian meatpackers basics

Deeper market context

Beef

US

Brazil

Swine

US

Brazil

Poultry

US

Brazil

Near-term cycle factors

Asian and Gulf demand

Grain prices

BRL exchange rate

Domestic demand cycles

Adding all together: summary by company and segment, plus valuation comments

Premier Annex: The Premier Annex to this article contains a deeper dive into the assets of each of the meatpackers by geography, segment, and link in the value chain. It also contains the data references and sources to follow the cycle forward.

Other articles on the topic

Meatpacking industry basics

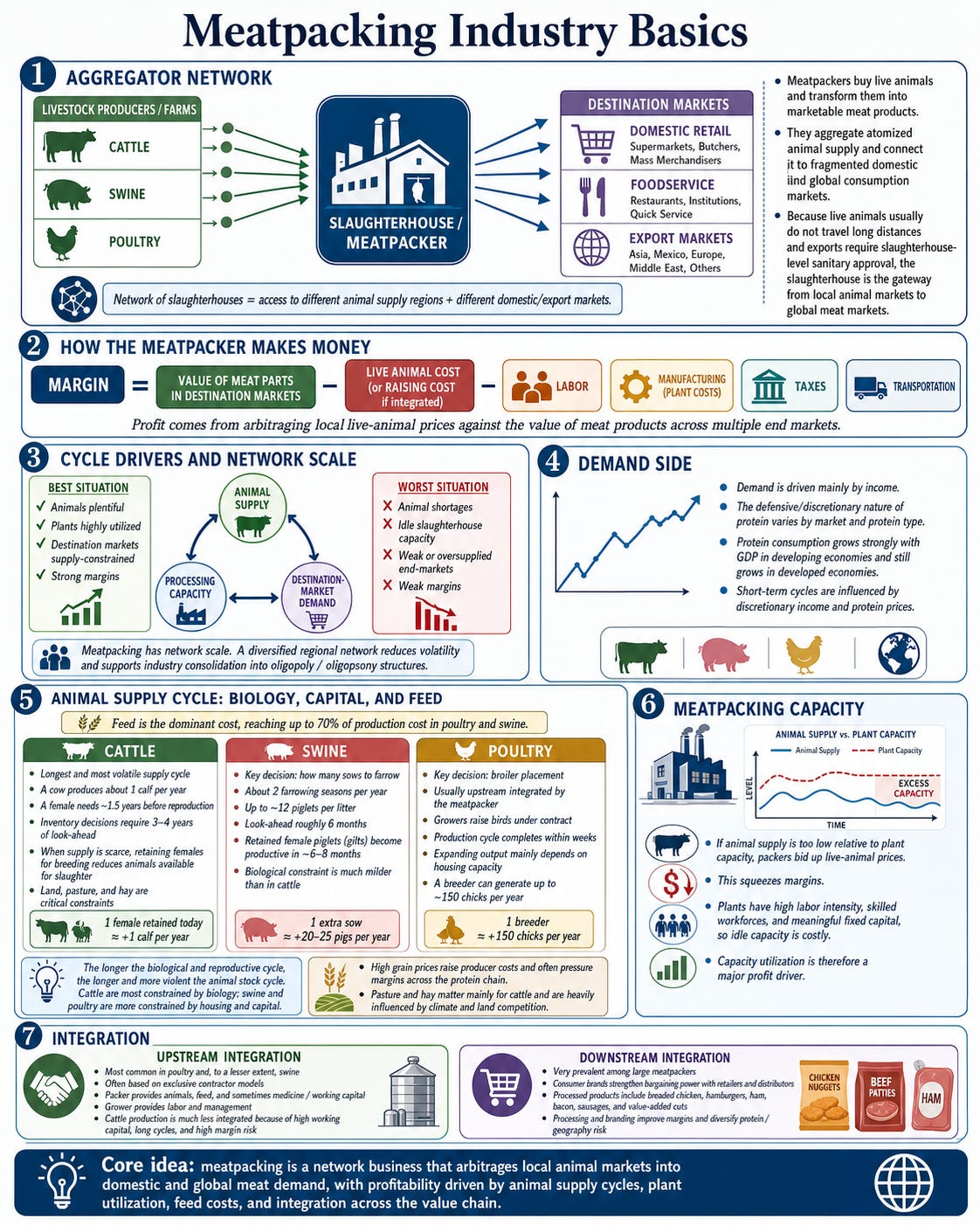

Aggregator network

The meatpacker is the aggregator of the animal industry into the meat industry.

At the core, a meatpacker is a company that buys live animals (cattle, poultry, swine) and transforms them into marketable meat products. This process happens primarily in a slaughterhouse. In the case of poultry and a little less for swine, meatpackers also integrate upstream into animal husbandry.

Their existence in the value chain is necessary because both the live animals market and the consumption markets are highly atomized. In addition, live animals do not usually travel long distances, and meat products have very strict sanitary regulations, with permissions for export at the slaughterhouse level. The slaughterhouse is therefore a point of access for a local animal market into the global meat consumption market.

The meatpacker builds a network of slaughterhouses, each with regulatory and reputational access to different domestic and global markets for consumption, and also to different animal supply markets. In the arbitrage between local animal prices and the different consumption markets’ prices for meat products, the meatpacker makes a margin, as measured by the difference between the price of the live animal (or the cost to raise an animal to slaughter weight in the case of upstream integration) and the value that can be obtained from its parts in the destination markets (of course, adding the labor, manufacturing, taxes, and transportation costs to bring the product to market).

Cycle drivers and network scale

The cycle of the meatpacker is protein-dependent (i.e., type of animal) and geography-dependent. That is, we talk about the cycle in Brazilian beef, Australian lamb, or US poultry. We could even bring the detail to regions within large producing countries. The cycle is determined by the availability of supply (number of animals), the processing capacity (measured in animal heads per day), and the demand/supply situation in the markets of destination of that particular region/slaughterhouse.

The best situation for a meatpacker is to be in a region where animals are plentiful, slaughterhouse capacity is fully utilized, and destination markets are supply-constrained. In such a context, the meatpacker can make the best margin. The opposite situation is having shortages of animals, idle slaughterhouse capacity, and depressed demand or oversupplied end-markets.

Because of the above, meatpacking is a business with a network scale. A meatpacker in a single region or with access to a few markets has a very volatile cycle. Therefore, when the cycle is bad in that region, he might get acquired by a larger player making money in another region. This is why meatpacking has slowly turned into a form of oligopoly/oligopsony. Oligopoly, because a few companies dominate the global demand markets, and oligopsony, because in any given region, only a few meatpackers have slaughterhouses to which a producer can sell.

Demand-side

The demand side of the cycle in each of the destination markets is influenced most heavily by income, although the degree of discretionary/defensive varies with each type of protein and the base level of wealth in each country. In the US, poultry might be defensive, but it’s probably more discretionary in Southeast Asia.

Secularly, protein in general is a highly sought-after product, and it is not reaching a saturation point, even in advanced economies. Meat consumption grows super-linearly with GDP in developing economies, but still grows in developed economies too. Peppered in this secular growth trend are cycles driven mainly by discretionary income and by protein prices (highly affected by grain prices).

Animal supply cycle: herd cycle, capital, and climate

The animal supply side of the cycle is different for each species, but in general, it is largely driven by three factors: the animal stock (herd/flock) cycle, the capital cycle (housing, fairly relevant for poultry/swine mainly), and the feed cycle (grains like corn or soybeans, or pasture/hay).

The producer makes a margin between the cost to feed the animal to slaughter age/weight and its price in the market alive in the slaughterhouse. There are other relevant costs like medicine, labor, lighting, heating, water, etc., but feed is the most important, reaching up to 70% of costs for poultry/swine.

When the aggregate stock of animals in a region is low relative to demand, the margin for the producer is good. The producer then decides to increase his stock. Conversely, when margins are bad, the producer wants to reduce his stock of animals.

How this increase happens depends on animal biology and affects the length of the supply cycles in each protein type (animal). The longer the lifecycle of an animal, and the longer the reproductive cycle of the animal, the longer and more volatile the animal stock cycle.

For cattle, the cycle is more relevant, lengthy, and violent. Cattle inventories take a long time to build because a cow can only have 1 offspring per year, and requires about 1.5 years before being able to have offspring. When animal supplies are low, producers might decide to sell the calves before they can have offspring, hindering the growth of the herd. The aggregate inventory of cattle decisions has to look 3/4 years in advance.

For swine, the key decision is how many females (sows) to put through pregnancy per season (2 seasons per year). This process is called farrowing. Each pregnant sow can have up to 12 pigglets (called a litter). Depending on that decision, the producer will have a specific pig crop per season, which can be fattened and then slaughtered. The decision is taken with 6 months of look-ahead. If the producer wants to increase his pig crop, he can retain some of the female piglets (called gilts) for about 6/8 months before they are ready to increase production. Further, one additional sow increases the yearly production by up to 20/25 animals. Therefore, the biological cycle is much shorter and much less relevant, as a constraint in capacity, than it is for cattle.

For poultry, the decision-maker (usually the meatpacker, upstream integrated) determines how many meat chickens (called broilers) to provide to a grower (a figure called broiler placement). The grower receives all inputs and puts labor and management under contract to bring the birds to slaughter weight. Within a few weeks, that cycle is finished. In order to increase the flock, the producer can simply place more broilers, obviously depending on housing capacity. Eventually, this will require having more breeders that lay fertile eggs, but again, the process from female increase to animal multiplication is fast because a breeder can generate as many as 150 chicks per year.

The animal stock cycle, therefore, exacerbates the supply cycle. When animals are scarce, they are most valuable as breeders, and therefore breeding decisions further reduce the availability of animals in the market for slaughter. When animals are plentiful, margins are low, and producers want to get rid of their stock, putting even more pressure on live-animal prices.

Notice the difference, however. For a cattle cow-calf producer to increase his calf crop by 1 per year, he has to spare 1 animal today from sale. A swine producer can increase his crop by 20 per year by sparing 1 female. A poultry producer has a 150x multiple on 1 female (which is actually not spared from the flock but rather bought from a different species).

In the case of poultry and swine, capital plays a larger role than the animal cycle. The animals require housing, and the decision to build housing is both more long-lived an harder to reverse than how many animals to house once it is built. Still, capital costs are not nearly as relevant to production as variable feed costs.

In the case of cattle, capital may not be as relevant, but land is, particularly for specific segments of production (cow-calf producers and early feeder producers) that require pasture or hay to eat. A big part of the current cycle in North American beef can be explained by land access and conditions.

Finally, the animal supply cycle is highly influenced by the cost and availability of feed, basically grains like corn and soybean for swine, poultry, and feedlot cattle, and pasture or hay for pasture cattle.

When grains are more expensive, protein is more expensive for the producer, and generally as well for the consumer. This impacts demand and generally pressures margins to the downside. Low grain prices are positive for the protein value chain in general. Even when they are high, accessing sufficient grain is generally not a problem, given that these are globally traded commodities and that the producer countries we are considering here have exportable surpluses.

Pasture or hay availability is relevant only for cattle production. Even in high feedlot-integrated systems like the US, calves and young adults usually need pasture or hay. Pasture and hay are much more influenced by climatic conditions, which can render them insufficient, therefore capping the size of the herd. Pasture and hay also compete for land with other, usually more capital-intensive uses of land, like grain crops.

Meatpacking capacity

A final component of the cycle is how much capacity for processing live animals and turning them into meat is available in a given region, compared to the supply of animals in that region.

This is particularly true for cattle and swine, where the packer might not be integrated upstream in the animal supply decision (like the case of poultry).

If, because of climatic, feed cost, or capital shortage reasons, there are too few animals to keep the capacity of a plant operating, the meatpackers will bid up the price of the animals, eating into their own margin. These plants have a skilled and numerous workforce that puts pressure on operating leverage, and generally have large capital layouts (asset utilization is close to 1x in these businesses).

Upstream integration

The meatpackers integrate the upstream producing link in the animal supply chain, particularly into poultry and swine.

The model is generally one of exclusive contractors. The packer provides the animal shortly after birth, the feed, and sometimes even covers other costs like medicine, and pays a fee for managing the feeding process until slaughter capacity. This is particularly true for poultry.

In other, less integrated models, the packer might still sign price contracts to provide safety to the producer, but might not provide the working capital, or carry the full margin risk.

Cattle producers are generally not integrated, or only moderately so. Cattle require high working capital outlays that are quite illiquid for up to a few years. Margin risk is pretty high. The meatpackers have generally shunned this link in the chain.

Downstream integration

Downstream integration is very prevalent among meatpackers.

Both JBS and MBRF have consumer brands in beef, poultry, and swine. This allows them to negotiate from a stronger position with retailers and distributors, given that consumers can place some value on the brands.

In the case of poultry and swine, particularly poultry, both companies also have large processed products brands and operations. This includes breaded chicken, hamburgers, ham, bacon, seasoned or value-added cuts, and sausages. In some consumer markets, like the US poultry industry, processed products make up the majority of the consumption of meat.

Downstream processing makes a lot of sense because it can capture the much better margins of building consumer brands, it can leverage the size and cost advantage of the meatpacker in segmented geographical consumer markets, and it is another way to diversify the risk of any specific protein and geographic cycle.

The Brazilian meatpackers

Today, there are three publicly traded Brazilian meatpackers: JBS, MBRF (the merger of Marfrig and BRF in 2025), and Minerva.

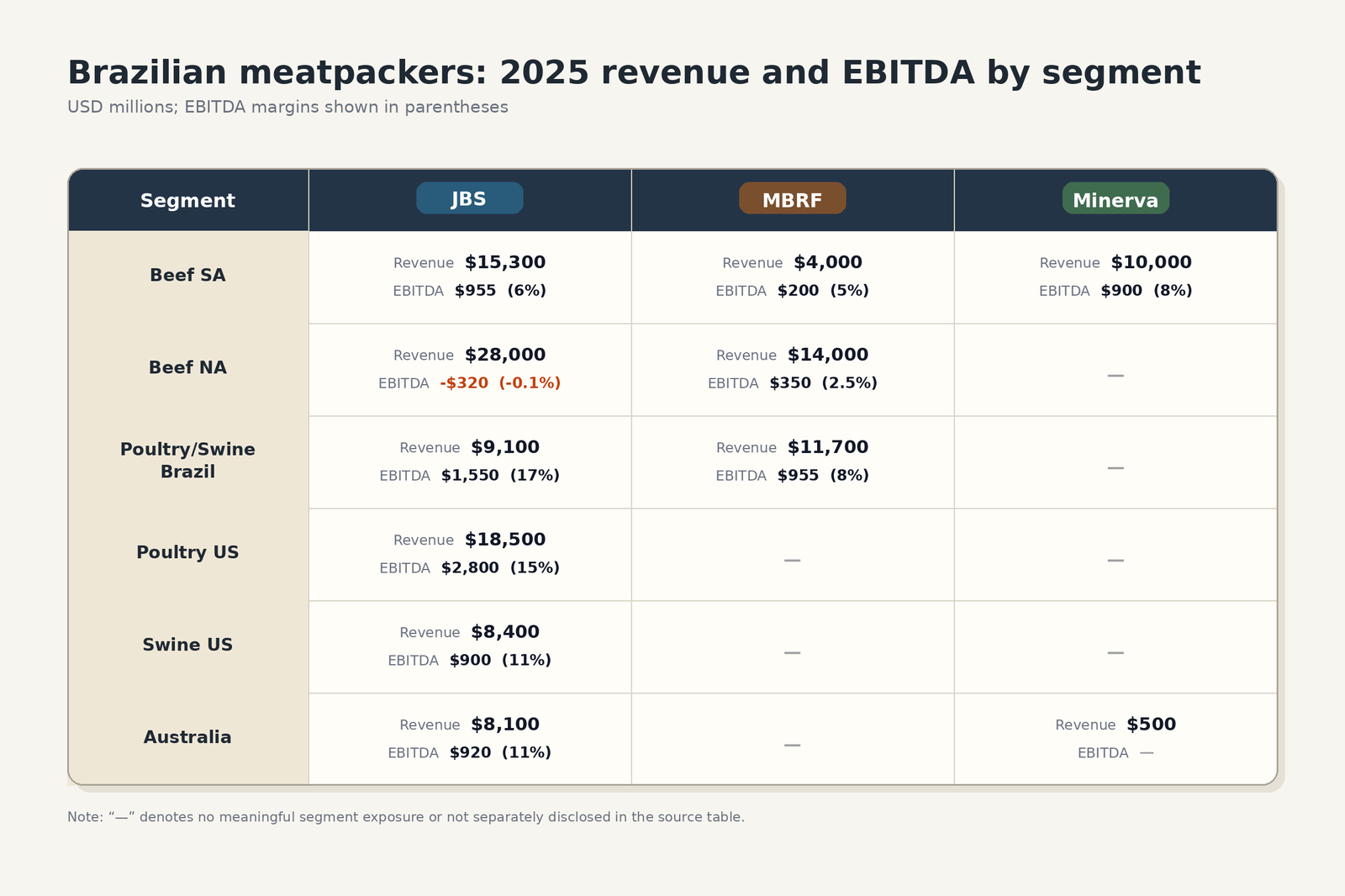

Each of them is about 3x larger than the other. Minerva has ~$10 billion in revenues, MBRF ~$30 billion, and JBS close to $90 billion.

Naturally, the largest players are more diversified, with JBS spanning all large protein groups along global geographies, and Minerva concentrated almost exclusively on cattle in South America.

Below are tables comparing their revenues and EBITDA by segment.

JBS is the largest, most diversified, and I would argue, strongest and highest-quality company in the group. They have a substantial operation in the US, representing more than half their revenues and half their EBITDA, across the three main proteins. In most of their segments, they have strong upstream and downstream integration. Their balance sheet position is the strongest, with most of its debt in USD, at fixed rates, and with long maturities.

MBRF follows very closely. The company is very strong in Brazil's poultry/swine markets through its Sadia and Perdigao brands. Their exposure in the North American beef market is almost as large as JBS's. In South American beef, they used to be a larger operator but sold a large part of their Brazilian, Uruguayan, and Argentinian operations to Minerva. Their balance sheet is not as pristine. They are fairly levered, with high exposure to BRL debt, which is expensive.

Finally, Minerva is a pure-play South American beef player, with approximately 60/70% of its capacity in Brazil. It is smaller and the most leveraged of the three.

Market context

Now that we have a basic understanding of where the companies operate and how a meatpacker makes money in each of the main protein markets, let us analyze the situation in each market, both by protein and by geography.

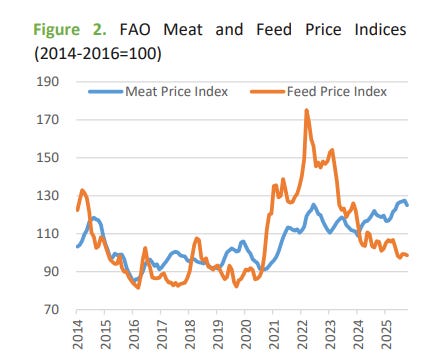

As a 30 thousand feet introduction, let us compare the FAO Meat and Feed price indexes for the past decade. We can easily observe how the 2020-2023 period of pressured margins (higher feed, slower meat) has been followed by a great period for meat, with falling feed prices and climbing meat prices. This is the context in which we find the industry today, a good profitability period across proteins and geographies (except US beef packing).

Beef

Beef is the most cyclical of the three proteins because of the compounded volatility of the herd cycle, the local pasture cycle, and the discretionary income cycle.

For the companies in this review, the two most important markets are the US and Brazil. In both geographies, the domestic market represents the majority of revenues, but exports are also a big consideration in the Brazilian cycle.

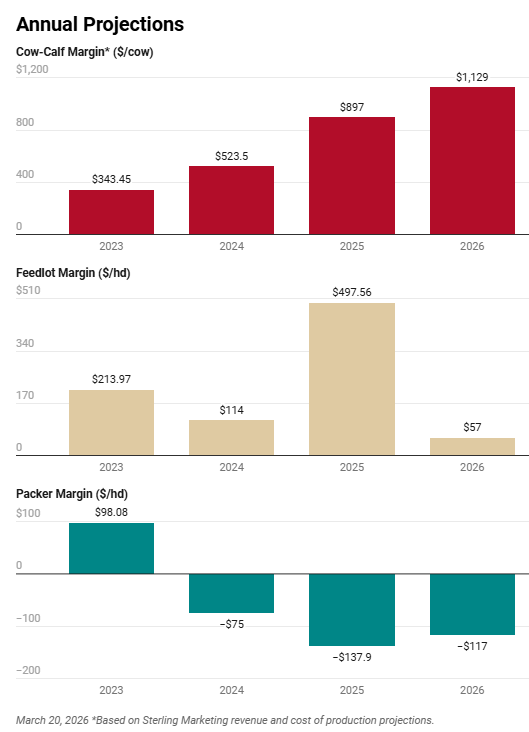

The US cycle has been a headache for meatpackers for a long time, already close to 5 or 6 years in a downcycle. It does not seem to be turning positive just yet. Capacity rationalization at the packer level might be needed.

At the same time, the Brazilian cycle, which had been a fantastic deliverer of profits and which still retains secular tailwinds, is starting to turn into a downcycle. Beef will be one of the tough spots for the meatpackers in 2026/27.

US

Secularly, the US is the largest producer and consumer market, but beef production has not grown since 1995. Structural conditions prevent this, including the cost of opportunity of pasture land, and potentially climate change.

Cyclically, the current herd downcycle has lasted 5 to 6 years, with minimal animal supply availability. Meatpacker capacity utilization has fallen by 15% since 2021/22, and meatpackers are operating at EBITDA breakeven levels or worse.

There are only a few cyclical indications of a herd inventory recovery cycle, and, secularly, doubts over the long-term beef-producing capacity in the US are still relevant.

A recovery in profitability will probably require meaningful capacity reductions.

The US is the largest producer of beef in the world (closely followed by Brazil).

It is by far the largest consumer market (~13 million tons per year), even larger than China’s (~11.5 million tons). It is therefore no surprise that US beef represents one of the largest segments for both JBS and MBRF.

The US market is predominantly domestic. Production covers about 90% of consumption, and the country is a net importer, but not by a huge amount. Therefore, the determinant of the cycle is primarily the local herd and the local demand circumstances.

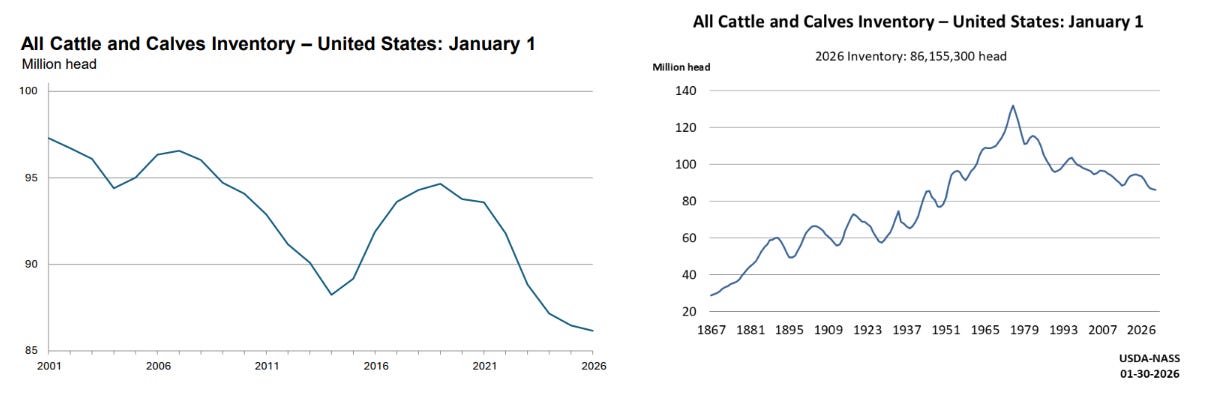

In terms of herd, the US has been in a prolonged negative cycle since at least the pandemic (left-hand side chart below), which, when seen from the perspective of history (right-hand side chart below), can even be considered secular. Cyclically or not, the US beef production has been basically flat since 1995.

There are several reasons for the US herd to shrink.

Secularly, other more intensive uses for land have become more profitable, especially agriculture, replacing pastures, thanks to the green revolution. The introduction of the feedlot as a link in the value chain allowed to produce more meat with the same or fewer animals. The productivity per animal in the US is twice or more than that of Brazil.

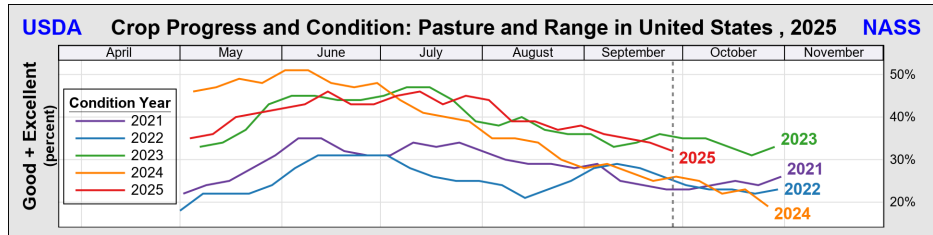

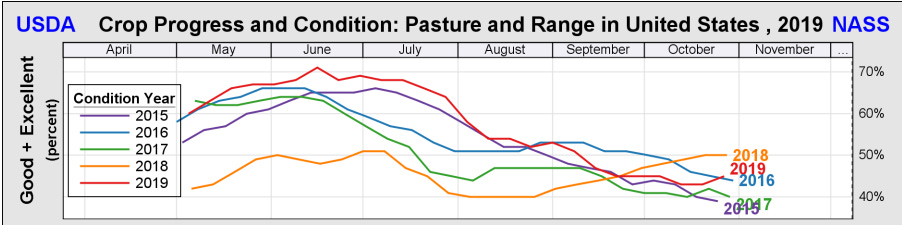

Cyclically, droughts in the US deteriorated pasture conditions in the Plains, where most of the cow-calf industry is based. The link in the chain that produces calves (called a cow-calf producer) is the most dependent on pasture conditions. When pastures are in worse condition, they can sustain fewer animals, leading to a lower intention to keep females to enlarge the herd next year.

In addition, the demand boom for meat during the pandemic led the next stage of the chain (called the feeders) to have a significant demand for calves. This stage buys a calf (female or male) from the cow-calf producer, and then feeds it (a mix of pasture and grains) until it is ready for slaughter. When demand for meat is high, and (as has been the case since 2023) grain prices are low, margins for feeders are high, meaning they are willing to pay up for calves. This leads to cow-calf producers having even a larger incentive to sell their calves before they can reproduce.

Today, there are still no signs that the herd cycle is turning, leading to continued supply tightening, at least as expected by the USDA.

We can observe that pasture conditions as an aggregate in the US have been significantly better in the past three years compared to 2020/21, but still almost 20pp below where the cattle cycle found its previous peak in 2015-2020.

On top of the cattle cycle, we also have capacity in the US beef packing industry, measured in slaughter head capacity per day, also called shackle space.

There is no aggregate US measure I was able to find.

However, the USDA reports for Federally Inspected Facilities show that the aggregate number of facilities has grown by 40% since 2019, and yet the slaughtered animal count has fallen by 12% since 2025. This speaks of idle capacity.

The increase in facilities (by number, not capacity) has occurred primarily among small plants of less than 10,000 heads per year, which grew 45% in that period. The animals processed in those plants also increased in line, around 48%. Still, as an aggregate, the segment represents less than 3% of the market. The increment could also represent simply a change in inspection (from state to federal).

The big losers of animal supply have been the large plants. For the facilities above 500 thousand heads per year, which represent 65% of the market, and which are probably the ones with the highest overhead costs to dilute, slaughter figures fell by 20%+. They lost more cattle (about 5 million animals) than the whole market (3.5 million animals). The number of facilities fell by a similar figure, from 22 to 18, or 18%.

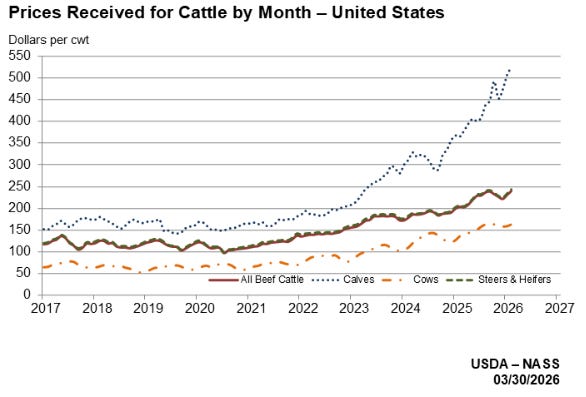

Finally, in terms of demand, the US remains insatiable. Despite the price of beef climbing by 85% since late 2020, consumption has expanded by almost 6% in aggregate terms. Because the production of meat has fallen by almost 10% in the same period, higher net imports have occupied part of that space.

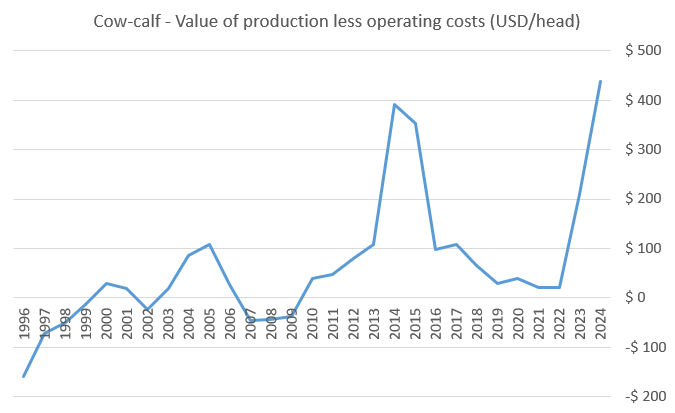

In conclusion, at least until 1Q26, the American consumer keeps demanding beef and pushing the price upwards, but the economics of cow-calf production have not yet reached a point where the herd is expected to grow and eventually recover the domestic supply of beef. In the meantime, with a low supply of animals and record capacity, meatpackers earn basically loss-making margins.

Because of the secular reasons pushing for a smaller herd, and the fact that cyclically, the herd does not seem to be close to turning yet, it seems that the only potential cyclical recovery will come from further plant closures.